Equipment Financing for Businesses: How It Works in 2026

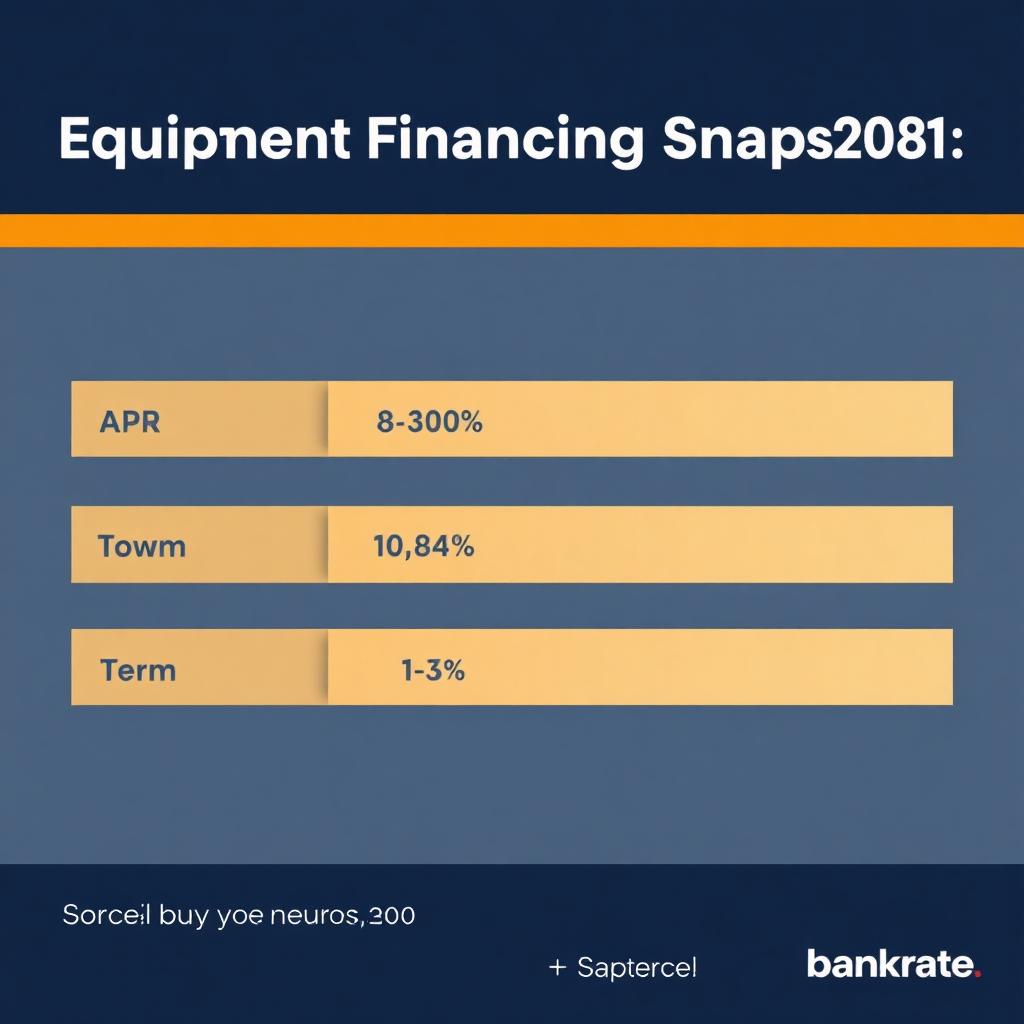

Equipment financing lets businesses purchase trucks, machinery, kitchen, medical, and shop equipment using the asset itself as collateral. Typical terms: 8–30% APR, 0–20% down, 24–84 month terms. Approval in 1–3 business days for most files. The asset's first-position UCC-1 lien reduces lender risk, which is why down payments are smaller than unsecured loans.

Equipment financing lets businesses purchase trucks, machinery, kitchen, medical, and shop equipment using the asset itself as collateral. Typical terms: 8–30% APR, 0–20% down, 24–84 month terms. Approval in 1–3 business days for most files. The asset's first-position UCC-1 lien reduces lender risk, which is why down payments are smaller than unsecured loans.

Key takeaways

- The equipment itself collateralizes the loan, reducing lender risk and your down payment.

- Typical down payment: 10–20% (sometimes 0% with strong credit) per NerdWallet.

- Term length: 24–84 months, matched to the equipment's useful life.

- APRs: 8–30% depending on FICO, time in business, and equipment type.

- Funding speed: 1–3 business days with a quote/invoice in hand.

- Equipment financing preserves working capital vs. cash purchase.

- Lease vs. loan: lease for technology equipment that depreciates quickly; loan for durable equipment you'll keep 5+ years.

Who this is for

Small business owners researching equipment financing for businesses who want a clear, advisor-quality overview before making a financing decision.

Operators comparing a current offer against alternative equipment financing for businesses options to confirm they are getting market-competitive terms.

First-time borrowers who want to understand the full equipment financing for businesses landscape before applying.

What you need to qualify

Typical requirements across the BizBee Funding partner network. Specific minimums vary by lender and product.

| Requirement | Typical standard |

|---|---|

| Time in business | 12+ months (some specialty lenders: 3 months) |

| Monthly revenue | $10,000+ ($25K+ for best rates) |

| Personal FICO | 600+ (700+ for best rates) |

| Equipment quote/invoice | Required from approved vendor |

| Down payment | 0–20% typical |

| Term | 24–84 months matched to useful life |

Best funding options

Product categories available through BizBee's lender network for this topic.

Equipment Loan

Ownership at payoff. Best for durable, long-life equipment.

Equipment Lease

Use-right only. Best for technology and short-life equipment.

Working Capital Loan

Use when equipment cost is small and speed matters more than secured rate.

SBA 504 Loan

For large equipment + real estate combinations. 5–7% APR per NerdWallet (June 2026).

How Equipment Financing Actually Works — and When to Lease Instead

Equipment financing is a secured loan in which the equipment serves as collateral. The lender files a first-position UCC-1 on the asset, the borrower makes monthly payments (typically over 24–84 months matched to useful life), and at payoff the lien is released and the title is clean. Because the asset secures the loan, approval is faster, down payments are smaller, and rates are usually lower than comparable unsecured term loans.

Down payments in 2026 typically run 10–20%, sometimes 0% for borrowers with strong FICO and established time in business (per NerdWallet). Heavier equipment with broader resale markets (trucks, construction, manufacturing) often qualifies for 0%–10% down; specialty equipment with limited resale markets requires 15%–25% down.

Rates range 8–30% APR. The cheapest tier (8–14%) goes to borrowers with 700+ FICO, 2+ years in business, and standard equipment categories. The middle tier (14–22%) covers most online equipment financing for established small businesses. The expensive tier (22–30%) applies to startups, lower FICO, or specialty equipment.

Lease vs. loan is the next decision. An equipment loan results in ownership at payoff — best for durable equipment you'll use 5+ years (truck, CNC machine, oven, lift). An equipment lease keeps the lender as the owner and gives you a use-right — best for equipment that depreciates quickly or that you'll want to upgrade in 24–48 months (laptops, POS systems, some specialized medical or print equipment). Operating leases also have different tax treatment than capital leases — ask your CPA.

Section 179 of the U.S. tax code lets businesses deduct up to $1,160,000 of qualifying equipment in the year of purchase (subject to phase-out and annual updates — verify the current year's limit with your CPA). This means the after-tax cost of equipment financing can be substantially lower than the headline APR suggests. Many borrowers who think they should pay cash actually benefit from financing once the tax math is run.

Used equipment is financeable too, but expect tighter terms: higher down payment (15–25%), shorter amortization (24–60 months), and a slightly higher rate. Reputable used-equipment financing requires a third-party appraisal or auction valuation and a clean title search.

What this typically costs

Representative 2026 cost scenarios. Your actual offer depends on credit, revenue, time in business, and lender.

| $100K equipment / 60 mo / 10% APR / 10% down | $1,912/mo · $114,800 total cost |

| $100K / 84 mo / 12% APR / 0% down | $1,765/mo · $148,260 total cost |

| $100K used equipment / 48 mo / 16% APR / 20% down | $2,266/mo · $108,800 total cost |

| $500K SBA 504 equipment + real estate | ~6.5% APR · 10–25 year amortization |

| Section 179 deduction (verify current limit) | Up to $1.16M qualifying equipment, year-1 deduction |

How to decide if this is right for you

Use this 5-step framework to narrow your shortlist before comparing specific offers.

-

1

Confirm the equipment is essential to revenue

Equipment financing is best when the asset drives top-line. Nice-to-have equipment doesn't justify the carrying cost.

-

2

Match term to useful life

Truck: 60–84 months. Restaurant equipment: 60 months. Tech/POS: 36 months (consider lease).

-

3

Get the Section 179 calculation from your CPA

The tax deduction can dramatically change the cash-vs-finance comparison.

-

4

Compare loan vs. lease for your specific situation

Loan for durable, lease for technology. Different tax and refresh implications.

-

5

Verify the vendor is on the lender's approved list

Most equipment lenders maintain vendor networks. Working with an approved vendor speeds approval and protects you on warranty/service.

When this makes sense

- The equipment is essential to revenue and depreciates predictably.

- Conserving working capital is more valuable than paying cash.

- The equipment's useful life is 24+ months.

- You can absorb a fixed monthly payment without straining cash flow.

- Your CPA confirms the tax treatment makes the after-tax cost work.

When to be careful

- When the term is much longer than the useful life of the equipment.

- When you're financing equipment you're not certain you'll use heavily.

- When the lender requires a personal guarantee on top of the equipment collateral and you have other PG exposure already.

- When the early-termination fee on a lease is buried in fine print.

- When you haven't asked whether Section 179 changes the cash-vs-finance math.

How this plays out in practice

Trucking company that financed correctly

Situation: Owner-operator with 3 trucks needed $145K for a new tractor. 3 years in business, $620K revenue, FICO 685.

Recommendation: Financed 84 months at 10.8% APR, 5% down. Monthly $2,310. The truck generates ~$8K/month in net contribution. Net positive monthly cash flow of $5,690 from day one.

Restaurant that should have leased

Situation: Owner financed a $42K POS system + tablets on a 60-month equipment loan at 14%.

Recommendation: Tech equipment has 24–36 month useful life. By year 4 they were paying for obsolete hardware. A 36-month operating lease with refresh option would have been a better match — same monthly cost, current equipment, no end-of-life problem.

The Section 179 surprise

Situation: Manufacturer was about to pay cash for a $180K CNC machine.

Recommendation: After CPA consultation: financed instead, deducted $180K in year 1 under Section 179, saved ~$54K in federal tax. The after-tax cost of financing was lower than paying cash — financing actually freed up working capital AND saved money.

Finance your next piece of equipment in 48 hours

Bring a quote or invoice — we'll match you with equipment lenders that specialize in your industry. Soft credit pull only. Down payments often 0–10% for established borrowers.

Frequently asked

Common questions

Key facts in one line

- Equipment financing requires 10–20% down on average per NerdWallet — sometimes 0% with strong credit.

- Equipment loan terms match useful life: 24–84 months is the standard range.

- APRs run 8–30% depending on credit, time in business, and equipment type.

- Section 179 lets businesses deduct up to $1.16M of equipment in year of purchase (verify current limit).

- The equipment's first-position UCC-1 lien reduces lender risk vs. unsecured loans.

Glossary

Terms worth knowing

- UCC-1

- A public lien filing the lender records to claim a security interest in the equipment until the loan is paid off.

- Operating lease

- A short-term lease in which the lessor owns the equipment and the lessee gets use rights. Common for technology equipment.

- Capital lease

- A lease structured to transfer ownership at end of term. Treated as a purchase for tax and accounting.

- Section 179

- A U.S. tax code provision allowing businesses to deduct the full purchase price of qualifying equipment in year of purchase, up to an annual cap.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.