Inventory Financing vs Purchase Order Financing

Inventory financing = loan secured by inventory you own/buy. PO financing = funder pays supplier directly to fulfill a confirmed customer PO. Inventory for restocking; PO for big confirmed orders.

Inventory financing uses inventory you already own (or are about to purchase) as collateral for a loan or line of credit. Purchase order (PO) financing pays a supplier directly to fulfill a confirmed customer order, you never touch the cash. Inventory financing fits restocking and seasonal buying; PO financing fits large confirmed orders you can't afford to fulfill out of cash.

Key takeaways

- Inventory financing: cash to you, secured by inventory.

- PO financing: cash to your supplier, secured by the customer's PO.

- Inventory financing usually 10%–30% APR; PO 1.8%–6% per month of fees.

- PO financing approves on the strength of your customer's credit, not yours.

- Both are short-term, designed for the inventory/order cycle.

Who this is for

Product-based businesses (wholesalers, distributors, e-commerce, importers) deciding which product fits.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Inventory financing | 6+ months, $15K+/mo, 600+ FICO, eligible inventory |

| PO financing | Confirmed PO from creditworthy customer, gross margin 20%+ |

The structural difference between inventory and PO financing

Inventory financing is a loan or line of credit where the inventory itself secures the debt. Cash flows to your bank account; you use it to buy or hold inventory; the lender files a UCC-1 lien on the inventory until repaid. Inventory financing fits restocking, seasonal buying, and holding finished goods in distribution.

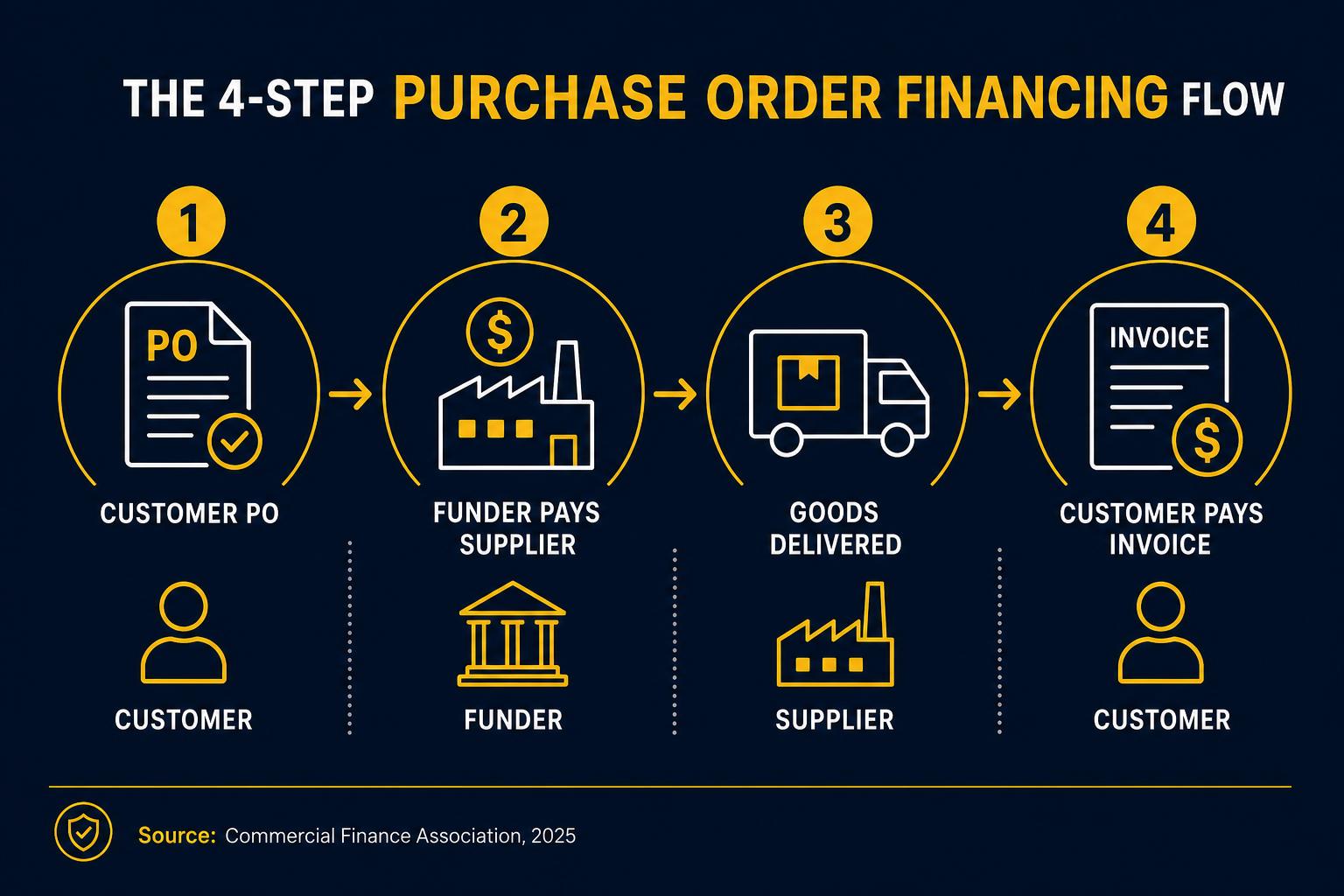

Purchase order (PO) financing is structurally different: the funder pays your supplier directly to fulfill a confirmed customer purchase order. You never receive cash. When your customer pays the invoice, the funder is repaid from those proceeds, often converting to factoring at the shipment stage. PO financing fits one-time confirmed orders too large to fulfill from cash on hand.

Cost structure compared

Inventory financing typically prices at 10%–30% APR depending on inventory liquidity, time in business, and credit (NerdWallet, 2025). Cost is annualized like any term loan or LOC, so longer holding periods cost more total dollars. Term is usually 6–24 months.

PO financing charges 1.8%–6% per month of the advanced amount (Nav, 2025), making it expensive on a monthly basis but typically short-duration (30–90 days). Total dollar cost on a 60-day cycle can be similar to or less than inventory financing for the same nominal use, but the structure is one-shot per PO rather than revolving.

Underwriting weights differ, your credit vs your customer's

Inventory financing underwrites on your business: credit, revenue, time in business, and the type of inventory. Fast-moving consumer goods are easier to finance than slow specialty items. PO financing underwrites primarily on your customer: their credit, payment history, and the likelihood of the PO being honored. A new or thin-credit business can often qualify for PO financing if the customer is a Fortune 500.

This is why PO financing is one of the few products genuinely available to early-stage product businesses, your customer's creditworthiness is doing the heavy lifting, not yours.

Worked example: $500K confirmed PO from a creditworthy retailer

Importer receives a $500K confirmed PO from a national retailer with 60-day payment terms. Cost of goods is $325K (65% of revenue), leaving $175K in gross profit. Importer has $80K in working cash, enough for half the supplier deposit but not the full build.

PO financing solution: funder pays the supplier directly for the $325K cost of goods, charging roughly 3% per month over the expected 60-day cycle from funding to customer payment — total fee approximately $19,500 (about 6% of the financed amount, or 3.9% of the customer's $500K revenue). When the retailer pays the invoice, the funder collects the financed principal plus fees and remits the remainder to the importer. Importer's net profit: $175K gross − $19,500 PO fee − operating overhead = roughly $135K–$145K net on the order, which would have been impossible to capture without the financing.

Inventory financing comparison on the same deal: an inventory loan against the finished goods after they arrive would advance roughly 50%–70% of the wholesale cost, leaving a 30%–50% gap that the importer still couldn't fund. Inventory financing fits restocking general inventory, not fulfilling a specific oversized PO. The two products are not interchangeable on a confirmed-PO scenario.

How seasonal cycles change which product wins

Inventory financing dominates for predictable seasonal builds. A consumer-goods brand stocking Q4 inventory in August or September has 90–120 days of expected hold time before sell-through, with no specific confirmed PO covering the full inventory. Inventory financing (or a LOC secured by inventory) is the right structure, annualized cost is lower than PO financing's monthly fee model when the carrying period exceeds 90 days, and the product fits the pattern of holding general inventory across many SKUs and many small customer orders.

PO financing dominates when a single confirmed order exceeds normal working capital. A custom furniture maker who suddenly receives a $200K hotel order, or a private-label manufacturer who lands a single oversized buyer order, can fund production through PO financing without disrupting normal operations. The order-specific structure means cost is incurred only when needed, on the specific deal, rather than as ongoing carrying cost.

Practical decision rule: under 30 days holding period = either product works. 30–90 days with a single confirmed customer = PO financing. 90+ days, multiple customers, predictable seasonal pattern = inventory financing or a LOC. The shorter and more customer-specific the cycle, the more PO financing tends to win.

Hybrid structures: pairing both with factoring

Many product businesses use a layered capital stack: a LOC or inventory facility for ongoing stock, PO financing for oversized one-time orders, and invoice factoring on the back end to bridge the receivables gap. Each product covers a different point in the cash-conversion cycle, and a thoughtful stack lets a $5M/year brand operate with $200K–$400K of standing working capital instead of $1M+.

Funders often coordinate. A common pattern: PO financing covers the supplier payment, converts to factoring at shipment so the importer's invoice to the customer is purchased at the same time, and the customer payment retires both legs simultaneously. BizBee partners with several funders who offer integrated PO + factoring under a single agreement to reduce fee stacking.

How underwriters actually compare the two products

Inventory financing and PO financing look adjacent on a product menu but underwrite to completely different risk frameworks. Inventory lenders care about borrower financial strength, inventory turnover (typically 4x+ per year per OCC commercial-lending guidance), and the existence of a perfected first-position UCC-1 on the inventory itself. PO funders care primarily about the end customer's commercial credit and the supplier's delivery reliability, the borrower's own balance sheet is secondary.

Cost differs proportionally. Inventory financing typically prices at Prime + 3–6% (roughly 11–14% APR per Nav 2026 benchmarks), with advance rates of 50–70% of inventory cost. PO financing prices at 2–6% per 30 days (effective 25–80% APR per NerdWallet 2026), with advance rates up to 100% of supplier cost. The PO premium pays for the production-risk gap inventory financing doesn't take.

Operational fit is the deciding factor for most borrowers. Steady-state inventory turnover for an established product line should be funded with inventory financing or an asset-based LOC. A specific oversized, confirmed customer order beyond standard stocking levels should be funded with PO financing on the front and invoice factoring on the back. Many product businesses run both products simultaneously, and BizBee advisors layer them rather than forcing borrowers to pick one.

What this typically costs

Typical 2026 cost ranges. Sources: NerdWallet, Nav, OCC.

| Inventory financing | 10%–30% APR |

| PO financing | 1.8%–6% per month of advanced amount |

How to decide if this is right for you

Five questions decide which product fits the situation.

-

1

Do you have a specific confirmed customer PO?

Yes, and you can't fulfill from cash = PO financing. No specific PO, general inventory need = inventory financing.

-

2

What's the gross margin on the PO?

PO fees consume 5%–15% of revenue. Margins under 20% won't survive. Inventory financing requires no such margin floor.

-

3

How long will the inventory or order cycle take?

PO financing breakeven is 30–90 days. Beyond that, inventory financing's lower monthly cost usually wins.

-

4

Is your customer creditworthy?

PO financing depends on customer credit. Risky customers get declined; large-cap or government customers approve easily.

-

5

Do you need ongoing flexibility or one-shot funding?

Inventory financing can be structured as a LOC; PO financing is one-PO-at-a-time.

When this makes sense

- Inventory financing: predictable restocking, seasonal buys, holding finished goods.

- PO financing: a confirmed customer order larger than your cash on hand.

When to be careful

- Inventory financing on slow-moving SKUs, you'll pay interest while it sits.

- PO financing on thin-margin orders — fees can erase profit.

How this plays out in practice

Distributor restocking ahead of season

Situation: Wholesaler buying $200K of recurring inventory across the year, holding 60–90 days per cycle.

Recommendation: Inventory financing as a LOC. Revolving access matches the recurring cycle; cost-of-capital lower than per-PO fees over a year.

Manufacturer with $500K confirmed PO from a Fortune 500

Situation: Startup manufacturer can't fund the $300K in supplier costs needed to fulfill a $500K PO with 40% gross margin.

Recommendation: PO financing. Customer credit carries underwriting; fees consume 6%–10% of revenue; gross margin survives comfortably.

Importer with seasonal stock + occasional big POs

Situation: Importer holds general stock and lands a $250K one-off PO from a major retailer 2x/year.

Recommendation: Both. Inventory financing as the base LOC for general stock; PO financing layered on the big one-off orders to avoid maxing the inventory line.

Distributor running both products in parallel

Situation: Industrial distributor holds ],M baseline inventory funded by an inventory line, then wins an unexpected $600K rush PO from a new account.

Recommendation: Keep inventory line in place for baseline; layer PO financing on the incremental order; factor the resulting invoice. Blended cost stays below either product run at higher single-line utilization.

Not sure which one fits?

Talk to a BizBee advisor, free, no obligation, no upfront fees.

Frequently asked

Common questions

Glossary

Terms worth knowing

- UCC-1 lien

- A public filing that gives a lender priority claim on specific business assets (e.g., inventory) as collateral.

- Recourse / non-recourse

- On factoring (which PO financing often converts to), recourse means you buy back unpaid invoices. Non-recourse shifts the credit loss to the funder.

- Advance rate (PO)

- The percentage of the PO value the funder will pay the supplier, typically 70%–90% depending on margin and customer credit.

- Inventory turnover

- How fast inventory sells through. Higher turnover = easier and cheaper inventory financing.

- Inventory turnover

- Cost of goods sold divided by average inventory. Inventory lenders typically want 4x+ annual turnover; slow-moving SKUs underwrite poorly.

- Field exam

- A physical or remote inventory audit conducted by the inventory lender, typically quarterly, to verify pledged inventory exists at the stated cost and condition.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.