What Is a Business Line of Credit?

A business line of credit is revolving capital you can pull from anytime up to your limit, pay back, and reuse, interest only on what you draw. Most are $10K–$500K with rates from roughly 8% APR (bank, prime) to ~28% APR (online, fair credit) depending on credit and revenue.

A business line of credit (LOC) is a revolving funding facility that lets a business borrow up to a pre-approved limit, repay what was used, and draw again, similar to a credit card but typically with lower rates, larger limits, and direct ACH transfers to a business bank account. You only pay interest on the amount you actually draw.

Key takeaways

- A line of credit is revolving, you can draw, repay, and re-draw without re-applying.

- You only pay interest on the funds you actually use, not the full approved limit.

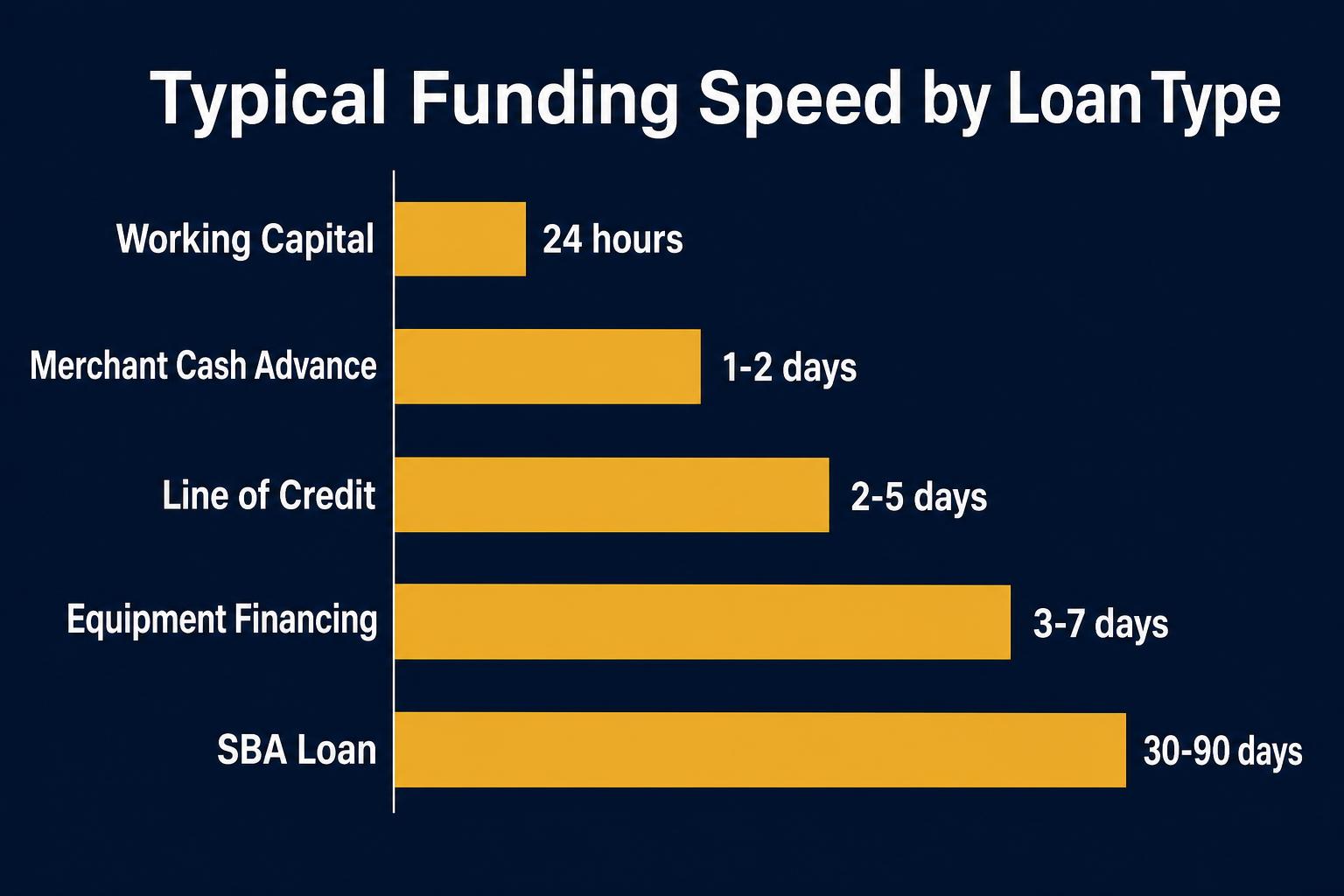

- Online LOCs typically fund in 1–3 days; bank LOCs can take 2–6 weeks.

- Most LOCs are unsecured for amounts under $100,000; larger limits may require collateral.

- Rates range from ~8% APR (bank, strong credit) to ~28% APR (online, fair credit).

- LOCs are best for short-term cash-flow gaps, payroll, and recurring small purchases — not long-term assets.

Who this is for

Established small businesses (12+ months) with $15K+ in monthly revenue that face uneven cash flow, seasonal swings, or unexpected expenses.

Owners who want capital standing by, without paying interest until it's needed.

What you need to qualify

Typical minimums across the BizBee partner network for a business LOC.

| Requirement | Typical standard |

|---|---|

| Time in business | 12+ months (some lenders accept 6+) |

| Monthly revenue | $15,000+ in consistent deposits |

| Personal credit | 600+ FICO (650+ for best rates) |

| Bank account | U.S. business checking with 3+ months of statements |

| Use restrictions | Working capital, payroll, inventory, marketing, not real estate |

Best funding options

Where a LOC fits relative to other BizBee products.

How a business line of credit actually works in practice

A business line of credit (LOC) is the most flexible product in small-business lending. After a single approval and credit limit assignment, the borrower can draw funds via ACH directly to their business checking account, repay them, and re-draw the same dollars again without re-applying. Interest accrues only on the drawn balance — not the full approved limit, which makes a LOC dramatically more efficient than a term loan for any business with intermittent cash needs.

Most modern LOCs from BizBee partners are revolving for 6–24 months at a time, then reviewed annually for renewal or limit increase. Bank-issued LOCs typically run $50K–$500K at 8%–13% APR; online LOCs run $10K–$250K at 18%–35% APR depending on credit and revenue. The cost gap is real but speed and approval flexibility usually favor online for borrowers under 700 FICO.

When a LOC outperforms every other product

A LOC is the right choice for recurring short-term cash-flow gaps: payroll between large customer payments, seasonal inventory restocks, or smoothing out 30–60 day receivables. The 'capital standing by, only pay if you use it' structure means you can pre-approve $100K and pay zero interest until the day you actually need it.

A LOC is the wrong choice for one-time lump-sum needs (a single equipment purchase or build-out). Term loans are usually 200–400 basis points cheaper than LOCs of equivalent size for a single, lump-sum, fully-drawn use. And a LOC is the wrong choice if you'll stay maxed out, at that point you're paying LOC pricing for what's effectively a long-term loan with worse flexibility.

What separates bank LOCs from online LOCs

Bank LOCs price cheaper (8%–13% APR), offer monthly billing, and tend to have unused-line fees. They require 700+ FICO, 2+ years in business, and 2–6 weeks to close. Online LOCs price higher (18%–35% APR), often bill weekly, and charge per-draw fees (1.5%–3%). They accept 600+ FICO, 12+ months in business, and close in 24–72 hours.

For borrowers who qualify for both, the bank LOC is almost always cheaper. For borrowers who don't qualify for a bank LOC yet, the online LOC bridges the gap until they do, typically 12–24 months of disciplined operating away.

How to manage a LOC so it stays open and grows over time

Disciplined LOC management compounds. The borrowers who see limit increases at renewal, and who keep the line through downturns — follow three rules. First, they pay each draw down to zero at least once per quarter, even if they re-draw the same day. Lenders read a 'paid-to-zero' cycle as healthy revolving behavior; sustained never-paid-down balances read as a term loan in disguise and trigger negative renewal action. Second, they hold utilization in the 30%–60% band on average. Below 30% signals the lender approved more credit than the borrower needs (which can mean a limit cut at renewal); above 75% signals cash stress. Third, they use the LOC for cash-flow timing (payroll, inventory, AR gaps) rather than long-term obligations.

Cost discipline matters more than headline rate. A LOC at 22% APR drawn for 14 days per month costs roughly the same in interest dollars as one at 12% APR drawn continuously, but the 22% APR version preserves liquidity by being mostly undrawn. Owners who chase the lowest headline APR and end up sitting maxed-out on a 12% line pay more total interest and have less flexibility than disciplined users on a 22% line.

At renewal time, three documents move the most weight: trailing-12 P&L showing revenue growth, a debt schedule confirming no new senior obligations, and 6 months of bank statements showing average daily balance trending up. Present these proactively rather than waiting for the lender to request them, borrowers who arrive at renewal with clean documentation see 25%–50% larger limit bumps than those who let the lender do the work.

What this typically costs

Approximate 2025–2026 rate ranges by lender type. Sources: Bankrate small-business LOC survey, Federal Reserve Small Business Lending Survey, NerdWallet 2025.

| Bank LOC (strong credit) | 8.00% – 13.00% APR |

| SBA CAPLines | Prime + 3.00% – 6.50% |

| Online LOC (mid credit) | 18.00% – 35.00% APR |

| Online LOC (subprime) | 40.00% – 60.00%+ APR |

| Typical draw fee | 1.50% – 3.00% per draw (online) |

| Origination fee | 0% – 3.00% of credit limit |

How to decide if this is right for you

Five questions decide whether a LOC is the right product for your specific need.

-

1

Is your need recurring or one-time?

Recurring (payroll smoothing, seasonal inventory) → LOC. One-time (single equipment buy, build-out) → term loan.

-

2

Will you draw the full limit or only portions?

Partial, intermittent draws → LOC wins on interest savings. Full draw, fully held → term loan is cheaper.

-

3

Do you qualify for a bank LOC (700+ FICO, 2+ years)?

If yes, start with your bank. Bank pricing typically beats online by 500–1,500 bps.

-

4

Can you comfortably service the minimum monthly interest?

Even on $0 drawn, some LOCs charge unused-line fees. Confirm before signing.

-

5

How fast do you need the line in place?

Bank LOC: 2–6 weeks. Online LOC: 24–72 hours. Match urgency to product.

When this makes sense

- You have recurring cash-flow gaps tied to receivables or seasonality.

- You want capital approved now and only pay if/when you use it.

- You make frequent small draws (payroll, inventory restocks) rather than one big purchase.

When to be careful

- You need a single large lump sum, a term loan is usually cheaper.

- You can't comfortably make the minimum monthly interest payment in a slow month.

- You're tempted to stay maxed-out — a LOC is for short-term gaps, not permanent debt.

How this plays out in practice

Restaurant smoothing seasonal swings

Situation: Restaurant with $90K/mo summer revenue dropping to $40K/mo in winter; needs $60K of cash-flow flexibility 4 months/year.

Recommendation: LOC. Pre-approve $75K limit, draw only during winter slow months, repay during summer peak. Interest-only on actual draws costs far less than a $75K term loan held year-round.

Services firm awaiting a $300K invoice

Situation: Consulting firm with a 60-day net-receivable from one client; needs $50K to cover payroll until paid.

Recommendation: LOC. One draw, one repayment when the invoice clears, no re-application for the next cycle.

Owner planning a single build-out

Situation: Retail business spending a one-time $150K on a new location with a clear 36-month payback.

Recommendation: Term loan, not a LOC. Single-use, fully-drawn, long-amortization needs are 200–400 bps cheaper as term loans than as LOCs.

B2B service firm building a payroll backstop

Situation: Marketing agency, $35K/mo revenue, payroll runs $18K every two weeks. Owner wants a safety net for one missed-client-payment month per year.

Recommendation: Pre-approve a $40K LOC and keep it undrawn. Annual cost in slow years: $0–$300 in unused-line fees. Cost of one bridged payroll missed without a LOC: lost staff, broken delivery, six-figure revenue risk. The LOC is insurance, not active capital.

See your LOC limit in minutes

Soft-pull pre-qualification with no impact to your credit score.

Frequently asked

Common questions

Key facts in one line

- Business lines of credit only charge interest on the amount actually drawn, not the full limit.

- Most online LOCs from BizBee partners fund within 24–72 hours of approval.

- Typical LOC limits range from $10,000 to $500,000, with first-time approvals averaging $25K–$150K.

Glossary

Terms worth knowing

- Revolving credit

- A credit facility that can be drawn, repaid, and re-drawn multiple times without re-applying. The opposite of an installment (term) loan.

- Draw fee

- A small fee (typically 1.5%–3% of the draw amount) some online LOCs charge each time funds are pulled. Bank LOCs usually don't have draw fees.

- Unused-line fee

- A small monthly or annual fee some lenders charge on the undrawn portion of a credit limit. Common on bank LOCs, rare on online LOCs.

- Annual renewal

- The yearly review during which a lender confirms continued access, may raise/lower the limit, and may reprice the line based on the borrower's current financials.

- Material adverse change (MAC)

- A contract clause allowing the lender to freeze new draws or accelerate repayment if the borrower's financial condition deteriorates meaningfully. Standard in nearly all LOC agreements.

- Utilization rate (LOC)

- Drawn balance divided by total approved limit. Sustained utilization above 75% can flag the file as cash-stressed; 30%–60% is the band most lenders associate with healthy use.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.