What Is a Working Capital Loan?

A short-term lump-sum loan (3–24 months) for operating expenses like payroll, rent, and inventory. Funds in 1–3 days, repaid via daily or weekly auto-debit. Costs range from ~8% APR (bank) to factor rates of 1.15–1.45 (online, fastest).

A working capital loan is a short-term business loan, typically 3 to 24 months, that delivers a lump sum of cash used to cover day-to-day operating expenses such as payroll, rent, inventory, utilities, and marketing. Unlike equipment or real estate loans, working capital loans are not used to buy long-term assets; they are designed to smooth out cash-flow timing.

Key takeaways

- Working capital loans cover everyday operating expenses, not long-term assets.

- Terms are short, typically 3 to 24 months, with fixed daily or weekly payments.

- Funding is fast: 24–72 hours from most online BizBee partners.

- Costs vary widely: bank loans from ~8% APR; online loans use factor rates (1.15–1.45) on the fastest products.

- Best used for ROI-positive needs: payroll to keep revenue flowing, inventory for a big order, or a marketing push.

Who this is for

Businesses with 6+ months of operating history and $15K+ in monthly revenue facing a temporary cash-flow gap.

Owners who need a known lump sum (not revolving capital) and can support a fixed repayment schedule.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Time in business | 6+ months |

| Monthly revenue | $15,000+ |

| Personal credit | 550+ FICO |

| Bank statements | 3–6 most recent months |

What working capital actually means, and when a working capital loan helps

Working capital is the cash a business needs to fund day-to-day operations between receiving customer payment and paying its own obligations. When customer payment timing lags behind payroll, rent, and supplier costs, the business has a working-capital gap. A working capital loan delivers a short-term lump sum (3–24 months) used to close that gap, never to fund long-term assets or to mask structural unprofitability.

The product is purpose-built for timing problems, not profitability problems. If revenue exists but lands 30–60 days after costs are due, working capital is the right answer. If revenue isn't there at all, working capital just delays a deeper restructuring conversation by a few months and adds debt to the problem.

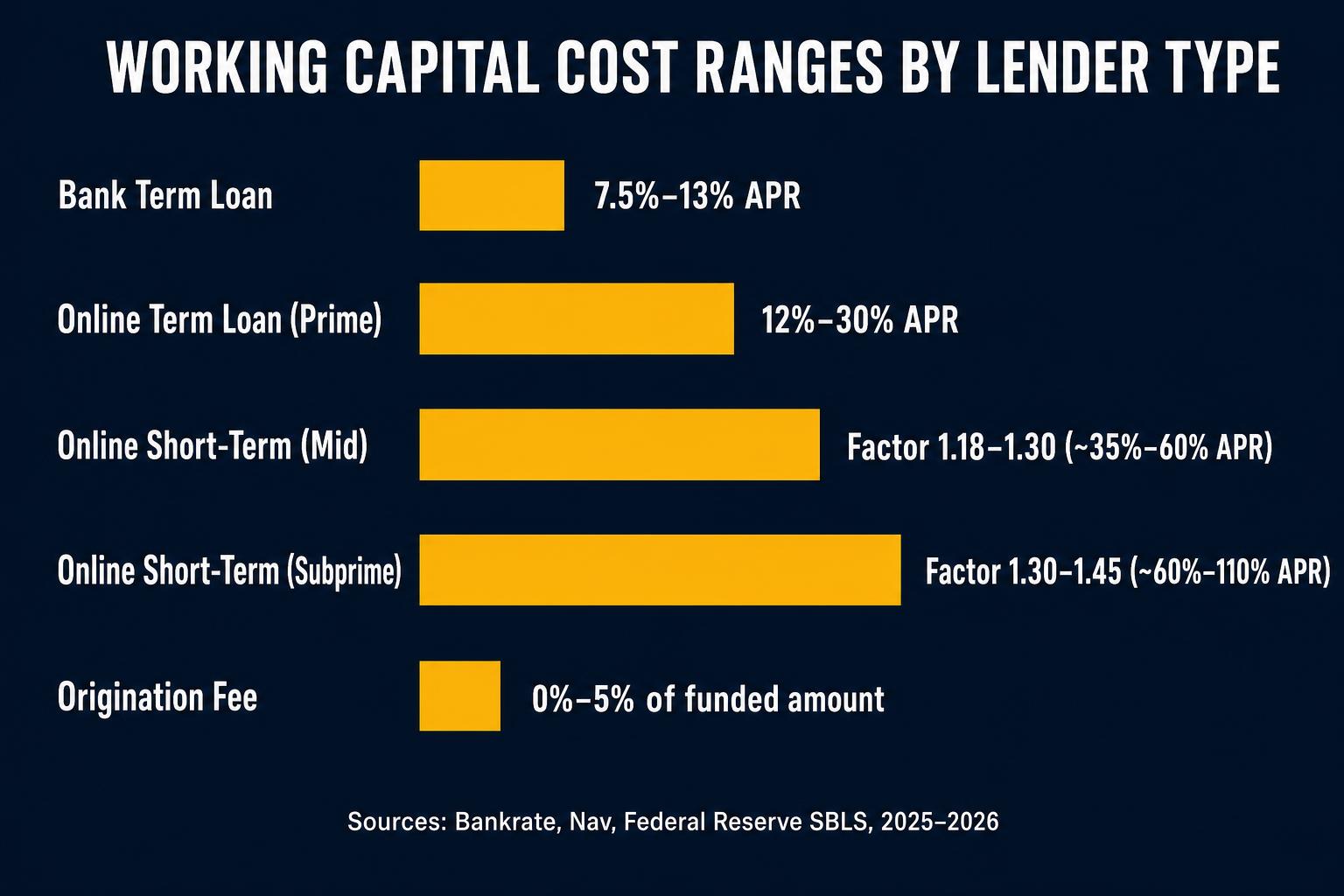

Working capital cost ranges in 2025–2026

Bank working capital term loans price 7.5%–13% APR for prime borrowers per Bankrate's 2026 small business lending data; the Federal Reserve Small Business Lending Survey put Q3 2025 fixed-rate averages between 6.99% and 7.38% on bank-issued working capital. Online prime working capital prices 12%–22% APR; mid-credit online runs 22%–35% APR. Short-term working capital advances use factor rates of 1.18–1.40, roughly 25%–60% APR equivalent depending on payback speed.

Funding speed and pricing move in opposite directions. 24-hour funding almost always uses factor pricing; 7–14 day funding usually gets APR pricing 200–800 bps cheaper. If timing allows, the slower product is materially cheaper.

How to size a working capital loan correctly

The correct size is the gap, not the maximum approval. Model your worst week's deposits against the daily or weekly debit on the new loan; the debit should never exceed 8–10% of worst-week deposits. Borrowers who size loans against their best month rather than their worst month account for most working-capital defaults.

Use the loan for ROI-positive needs: payroll that keeps revenue flowing, inventory for a specific order, or a marketing push with measurable conversion. Avoid using working capital to plug recurring monthly shortfalls, that's a profitability problem, not a timing one.

Daily-debit vs. weekly-debit vs. monthly-payment structures

Repayment cadence is the most underappreciated variable in working capital pricing. Daily ACH debit is the dominant structure for sub-12-month online loans because it gives the lender real-time visibility into business health, a missed daily debit triggers an immediate underwriting review. The trade-off for the borrower is intense cash-flow discipline: every business day, a fixed amount disappears from the operating account.

Weekly-debit structures (typically 12–18 month terms) give the borrower 4 days of cash accumulation between payments — much easier on operations, slightly more expensive in headline rate. Monthly-payment structures (24+ months) are the cheapest and most cash-flow-friendly but require stronger underwriting: typically 650+ FICO, 2+ years in business, and bank-grade documentation.

Pick the longest cadence your file qualifies for. The cash-flow benefit of monthly over weekly, or weekly over daily, almost always outweighs the modest pricing premium for borrowers with seasonal or lumpy revenue. The reverse is true only for borrowers with extremely consistent daily card sales (some retail, restaurant, e-commerce), where daily debits genuinely match the revenue pattern.

What this typically costs

Typical 2025–2026 working capital cost ranges. Sources: Bankrate, Nav, Federal Reserve SBLS.

| Bank term loan | 7.50% – 13.00% APR |

| Online term loan (prime) | 12.00% – 30.00% APR |

| Online short-term (mid) | Factor 1.18 – 1.28 (≈25%–45% APR equivalent) |

| Online short-term (subprime/fastest) | Factor 1.28 – 1.40 (≈45%–60% APR equivalent) |

| Origination fee | 0% – 5% of funded amount |

How to decide if this is right for you

Five gates before signing a working capital loan.

-

1

Confirm the problem is timing, not profitability

If revenue covers costs over a 90-day window but timing creates gaps, working capital fits. If costs exceed revenue, fix that first.

-

2

Size against worst-week deposits

Daily/weekly debit should never exceed 8–10% of your weakest week's deposits. Larger debits compound risk.

-

3

Choose APR over factor whenever timing allows

If you can wait 7–14 days, APR-priced term loans are 200–800 bps cheaper than factor-rate short-term advances.

-

4

Verify use is ROI-positive

Use proceeds for payroll/inventory/marketing where each dollar produces more than the cost of capital.

-

5

Map the payoff to a specific revenue event

Best-case payoff is tied to a measurable inflow (customer payment, season, order fulfillment).

When this makes sense

- You have a specific dollar amount you need now and can repay on a fixed schedule.

- Cash-flow timing — not profitability, is the actual problem.

When to be careful

- You're using it to plug structural losses (not timing gaps). Working capital won't fix an unprofitable business.

- Daily-debit payments could squeeze a fragile cash position. Model the daily payment against worst-week deposits.

How this plays out in practice

Retailer pre-funding holiday inventory

Situation: Retail business needs $80K in September for Q4 inventory; expects $200K in Nov–Dec sales.

Recommendation: 12-month working capital term loan at 18–24% APR. Inventory ROI is well above cost; payoff tied to known revenue event.

Service firm covering payroll between invoices

Situation: Consulting firm has $50K of net-30 invoices outstanding; needs $30K for two weeks of payroll.

Recommendation: Short-term 3–6 month working capital advance OR a LOC if pre-approved. Sized to actual gap, paid off when the invoice clears.

Restaurant with declining revenue

Situation: Restaurant deposits down 30% over six months; owner considering $50K working capital to 'bridge.'

Recommendation: Do not borrow. This is a profitability problem, not a timing one. Restructure operations first.

Contractor pre-funding a $400K signed project

Situation: Commercial GC has a $400K signed contract starting in 30 days; needs $120K upfront for materials and crew before first draw arrives in week 8.

Recommendation: Use a 6-month working capital advance sized to the actual gap. Tie payoff plan to the week-8 draw. Avoid stretching the loan past 9 months, the project should self-fund well before then.

See what working capital you qualify for

Real offers from BizBee partner lenders in minutes, soft pull only.

Frequently asked

Common questions

Glossary

Terms worth knowing

- Working capital

- Current assets minus current liabilities, the cash a business has on hand to fund operations after near-term obligations are met.

- Cash-flow gap

- The period between when costs are due and when corresponding revenue is collected. The core problem working capital loans are designed to solve.

- Factor rate (working capital)

- A multiplier (typically 1.18–1.40) used on short-term working capital advances. Total payback = advance × factor.

- Daily ACH debit

- The fixed-dollar amount automatically pulled from a business checking account each business day to repay a short-term working capital advance.

- Holdback percentage

- The share of daily deposits a lender effectively claims through debits. Industry-safe holdbacks stay under 10%; holdbacks above 20% signal cash-flow stress and elevated default risk.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.