Best Working Capital Loan Options for Small Business

The best working capital loan options for most small businesses are: (1) a business line of credit (10%–60% APR per NerdWallet, 2026) for recurring, revolving cash-flow gaps; (2) a short-term working capital loan (9%–45% APR) for one-time fixed needs; (3) invoice factoring for B2B receivables; (4) revenue-based financing (1.10–1.35 factor) for variable revenue; and (5) a merchant cash advance (40%–350% factor-equivalent APR) only when other channels have been exhausted. The right choice depends on whether the gap is recurring or one-time, and how predictable monthly revenue is.

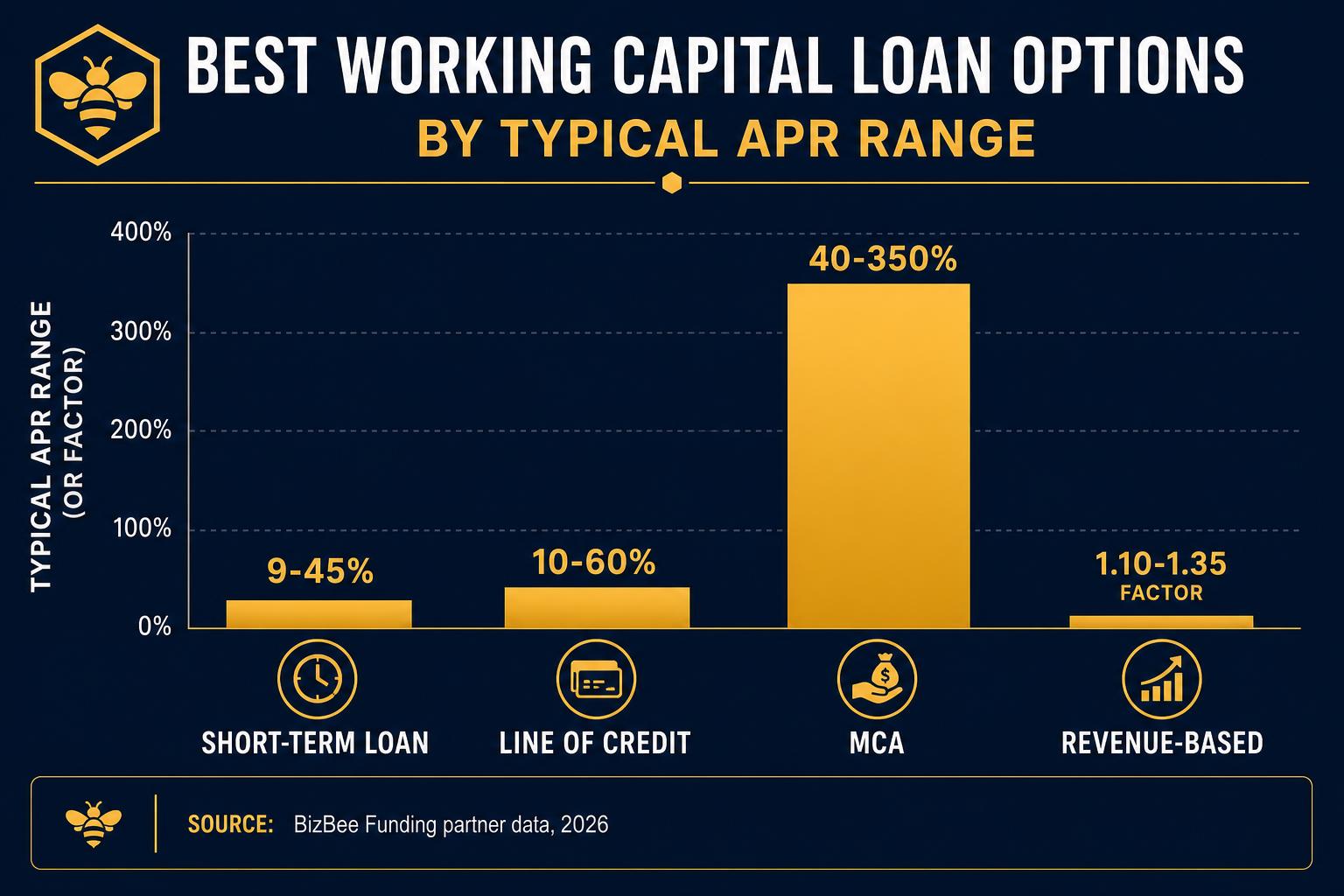

Working capital loans cover day-to-day operating expenses, payroll, rent, inventory, marketing, vendor bills, rather than long-term assets. The five mainstream working-capital products available to small businesses in 2026 are: business line of credit, short-term working capital loan, invoice factoring, revenue-based financing, and merchant cash advance. A business line of credit (typically 10%–60% APR per NerdWallet, 2026) is the most flexible and lowest-cost option for businesses with consistent revenue and 600+ FICO, you draw only when needed and pay interest only on the balance. A short-term working capital loan (9%–45% APR) makes sense when you need a fixed lump sum for a defined project. Invoice factoring fits B2B operators with outstanding receivables. Revenue-based financing (1.10–1.35 factor over 6–18 months) makes sense for variable revenue, and an MCA (40%–350% factor-equivalent APR per Bankrate, 2026) should be a last resort because the daily debit can choke cash flow. BizBee Funding compares all five channels in one soft-pull application.

Key takeaways

- Line of credit is best for recurring cash-flow gaps, pay interest only on the drawn balance.

- Short-term working capital loan (9%–45% APR) is best for one-time fixed needs.

- Invoice factoring converts outstanding B2B receivables into cash within 1–3 days.

- Revenue-based financing fits businesses with variable monthly revenue (seasonal, ecommerce).

- MCAs (40%–350% factor-equivalent APR) should be a last resort, not a starting point.

- Compare APR (or factor-equivalent APR), total cost of capital, and payback period — not the monthly payment alone.

- Speed-to-funding ranges from same-day (LOC, MCA) to 3–7 business days (term loan).

Who this is for

Operators covering a payroll, rent, or vendor gap inside the next 7–14 days.

Owners deciding between a revolving line of credit and a fixed-term working capital loan.

B2B businesses with outstanding receivables that could fund operations if collected faster.

Seasonal or variable-revenue businesses comparing flexible vs. fixed-payment structures.

Anyone who has been pitched an MCA and wants to see whether a lower-cost option exists.

What you need to qualify

Typical qualification thresholds across the five mainstream working capital channels. BizBee can usually find a match starting at 6 months in business with $10K+ monthly revenue.

| Requirement | Typical standard |

|---|---|

| Business line of credit | 600+ FICO · 6+ months in business · $10K+ monthly revenue |

| Short-term working capital loan | 550+ FICO · 6+ months in business · $15K+ monthly revenue |

| Invoice factoring | B2B invoices to creditworthy customers · 500+ FICO often OK |

| Revenue-based financing | 500+ FICO · 3–6 months of consistent monthly revenue · $10K+/mo |

| Merchant cash advance | 500+ FICO · 3+ months in business · $10K+ monthly revenue |

Best funding options

The five mainstream working capital products, ranked by typical all-in cost. Use the lowest-cost product you qualify for and that fits the use of funds.

Business Line of Credit

Revolving credit you draw from as needed and only pay interest on the drawn balance. Best for recurring or unpredictable cash-flow gaps. Typically 10%–60% APR per NerdWallet (2026).

Short-Term Working Capital Loan

Fixed lump sum repaid over 3–18 months. Best when the use of funds is a defined one-time project. Typically 9%–45% APR.

Invoice Factoring

Sell outstanding B2B receivables for immediate cash at a 1%–5% per-month discount. Best for B2B operators with 30/60/90 day receivables.

Revenue-Based Financing

Repaid as a fixed percentage of monthly revenue. Best when revenue varies month to month. Typical factor 1.10–1.35 over 6–18 months.

Merchant Cash Advance

Last-resort daily-debit advance against future card sales. Typically 40%–350% factor-equivalent APR per Bankrate (2026). Only use when other options are exhausted and the ROI clearly covers the cost.

Seasonal Working Capital

Funding structured around seasonal revenue cycles, repayment timed to in-season cash flow.

How to Match the Right Working Capital Product to Your Cash-Flow Gap

The single biggest mistake we see in working capital decisions is treating all five products as interchangeable. They are not. The cost of capital varies by roughly a factor of 10 across the channels, a $50,000 working capital need can cost anywhere from ~$2,500 (line of credit drawn briefly) to ~$25,000 (MCA over 6 months). The right product is the one that matches the shape of the cash-flow gap, not the one that gets approved fastest. Recurring or unpredictable gaps (slow seasons, staggered receivables, seasonal inventory buys) fit a line of credit because you only pay interest on what you draw. One-time, fixed-cost projects (a new piece of equipment that does not qualify for equipment financing, a marketing push, a build-out) fit a short-term working capital loan because the payment schedule is predictable and the all-in cost is locked.

B2B operators with consistent outstanding receivables should look at invoice factoring before any debt product, you're not borrowing, you're selling an asset you already own at a small discount. The all-in cost on factoring is typically 1%–5% per 30 days outstanding, which beats almost any short-term loan. Variable-revenue businesses (ecommerce, seasonal retail, restaurants with weather-driven traffic) should consider revenue-based financing because the repayment flexes with sales, there's no fixed monthly burden that can choke cash flow in a slow month.

Merchant cash advances belong in the last-resort category. A 1.30 factor over 6 months looks like '30% cost' to many operators, but the factor-equivalent APR is usually 60%–120% because the principal is repaid daily. Per Bankrate (2026), MCA factor-equivalent APRs run 40%–350%. The daily debit also reduces the cash flow available to fund operations, which can create a doom loop where the business takes a second MCA to cover the debits on the first. Before signing an MCA, confirm in writing that no other channel on this list is available — and if you do take one, plan an early payoff or refinance the moment your file qualifies for a lower-cost product.

Cost, Speed, and Risk: The Real Trade-Offs Across the Five Channels

Speed-to-funding ranges from same-day (existing line of credit, MCA) to 1–3 business days (invoice factoring, revenue-based, new short-term loan) to 3–7 business days (larger working capital term loans and SBA-backed options). Cost ranges from roughly 10%–18% APR (LOC with strong credit), 9%–45% APR (short-term term loan), 12%–35% factor-equivalent APR (factoring depending on receivable terms), 20%–60% factor-equivalent APR (revenue-based), and 40%–350% factor-equivalent APR (MCA). Term ranges from 30 days (factoring per invoice) to 6–18 months (most working capital products) to 36 months (larger working capital term loans).

The biggest hidden risk across all five products is stacking: taking a second or third working capital product on top of an existing one. Stacking is the leading cause of cash-flow distress we see at BizBee, the combined daily/weekly debits eventually exceed the safe envelope. If you already have one working capital product and need more, the right move is almost always to consolidate first (lower the combined debit) before adding new capital. We routinely consolidate 2–3 MCAs into a single SBA-backed or longer-term product, cutting the monthly outflow by 40%–60% and freeing up cash for actual operations.

Personal credit impact varies by channel. Lines of credit and term loans typically run a hard pull at close. Factoring and many MCAs are softer because the underwriting weighs receivables or bank revenue more than FICO. Revenue-based products fall in between. Initial prequalification through BizBee uses a soft credit pull across all five channels at once, you see real offers without a hard inquiry, then choose the single product to formally close on.

What this typically costs

What $50,000 of working capital typically costs across the five mainstream channels. Use as benchmark for any specific offer you receive.

| Line of credit drawn 3 months ($50K) | 12%–18% APR · ~$1,500–$2,250 interest |

| Short-term working capital loan ($50K, 12 mo) | 9%–45% APR · ~$2,500–$12,500 interest |

| Invoice factoring ($50K, 45 days) | 1.5%–4% discount · ~$750–$2,000 fee |

| Revenue-based ($50K, ~12 mo) | Factor 1.20–1.35 · $10,000–$17,500 total fee |

| Merchant cash advance ($50K, 6 mo) | Factor 1.30–1.45 · $15,000–$22,500 total fee |

How to decide if this is right for you

Five-step framework for choosing the right working capital product.

-

1

Describe the gap precisely

Is it a recurring cash-flow gap (favors LOC), a one-time fixed need (favors short-term loan), an outstanding receivable (favors factoring), or a revenue-timing mismatch (favors revenue-based)?

-

2

Set the cost ceiling

Calculate the expected ROI on the borrowed capital. The all-in cost of the product (APR or factor-equivalent APR) should be a fraction of the expected return, ideally 30% or less of projected ROI.

-

3

Rank products by cost

LOC < short-term loan < factoring < revenue-based < MCA, in most cases. Always pick the lowest-cost product you qualify for that fits the gap.

-

4

Check the debit schedule

Daily and weekly debits must fit the slowest revenue week of the year, not the average. If the debit consumes more than 8%–10% of daily revenue, the product is too expensive for the business.

-

5

Plan the exit

Every working capital product should have a defined payoff or refinance plan. Set a date to re-shop the file for a lower-cost product as your operating history and credit improve.

When this makes sense

- When the use of funds has a measurable ROI greater than the all-in cost of capital.

- When the gap is genuinely short-term (under 18 months) and not a permanent revenue shortfall.

- When the debit or payment schedule fits your slowest revenue week without straining operations.

- When you've compared at least three of the five mainstream channels in writing.

- When the product matches the shape of the gap (revolving vs. fixed, variable vs. flat payment).

When to be careful

- When you're funding ongoing operating losses rather than a defined growth investment.

- When the offer is the second or third working capital product on top of an existing one (stacking).

- When the daily/weekly debit exceeds 8%–10% of daily revenue on a normal week.

- When the only quoted product is an MCA and you haven't checked LOC, factoring, or short-term loan options.

- When the lender will not provide a written APR or factor-equivalent APR.

How this plays out in practice

Real-world example: the contractor who refinanced two MCAs into a line of credit

Situation: A specialty contractor had two MCAs totaling $80K in outstanding balance with combined daily debits of $1,100. Monthly revenue was steady at $180K but cash flow was choking.

Recommendation: We placed a $150K line of credit at 14% APR. He used $80K to pay off both MCAs (saving the daily debit) and held $70K as standby capacity. Monthly outflow dropped from ~$24K to ~$1,200 interest on the drawn balance. Annual cost savings: roughly $35,000.

Real-world example: the seasonal retailer who used revenue-based financing

Situation: A retail business doing 60% of revenue in Q4 needed $40K for Q3 inventory but couldn't support fixed monthly payments through the slow Q2.

Recommendation: We placed a $40K revenue-based advance at a 1.25 factor with repayment at 8% of monthly revenue over 11 months. Slow-month payments were ~$1,600; peak-month payments were ~$6,000. Total cost: $10,000. A fixed term-loan payment would have strained the slow months and risked a missed payment.

Real-world example: the B2B services firm that used factoring instead of a loan

Situation: A consulting firm had $120K in outstanding 60-day invoices to creditworthy enterprise clients and needed $50K immediately for a new hire.

Recommendation: We placed an invoice factoring facility at 2.5% per 30 days. They advanced 85% of $60K in invoices ($51K) and paid roughly $1,500 in fees per 30-day cycle. Total cost over 60 days: ~$3,000, versus ~$9,000 in interest if they had taken a $50K short-term loan.

Compare working capital options in one soft-pull application

Apply once and we'll match you against lines of credit, short-term loans, factoring, revenue-based, and (only when it makes sense) MCAs across our partner network. See real APRs and factor rates in writing before you commit.

Frequently asked

Common questions

Key facts in one line

- Line of credit APRs typically run 10%–60% per NerdWallet (2026); MCAs run 40%–350% factor-equivalent APR per Bankrate.

- The all-in cost of $50K in working capital can vary 10x across the five mainstream channels.

- Stacking multiple working capital products is the leading cause of cash-flow distress in small business.

- Invoice factoring at 1.5%–4% per 30 days is often cheaper than a comparable short-term loan for B2B operators.

- Revenue-based financing fits variable-revenue businesses because repayment flexes with sales.

- MCAs should be a last resort, not a starting point, confirm in writing that no other channel is available first.

Glossary

Terms worth knowing

- Working capital

- Cash available to fund day-to-day operating expenses, payroll, rent, inventory, vendor bills — rather than long-term assets.

- Line of credit

- Revolving credit you draw from as needed; you pay interest only on the drawn balance.

- Factor-equivalent APR

- The annualized cost of a factor-rate product (MCA, revenue-based) expressed as an APR for apples-to-apples comparison with traditional loans.

- Invoice factoring

- Selling outstanding B2B receivables to a third party for immediate cash at a small discount.

- Stacking

- Taking a second or third working capital product on top of an existing one, the leading cause of cash-flow distress.

- Daily debit

- Automated daily ACH withdrawal used by MCAs and some short-term loans to collect repayment from the business bank account.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.