Advantages of Online Business Lenders

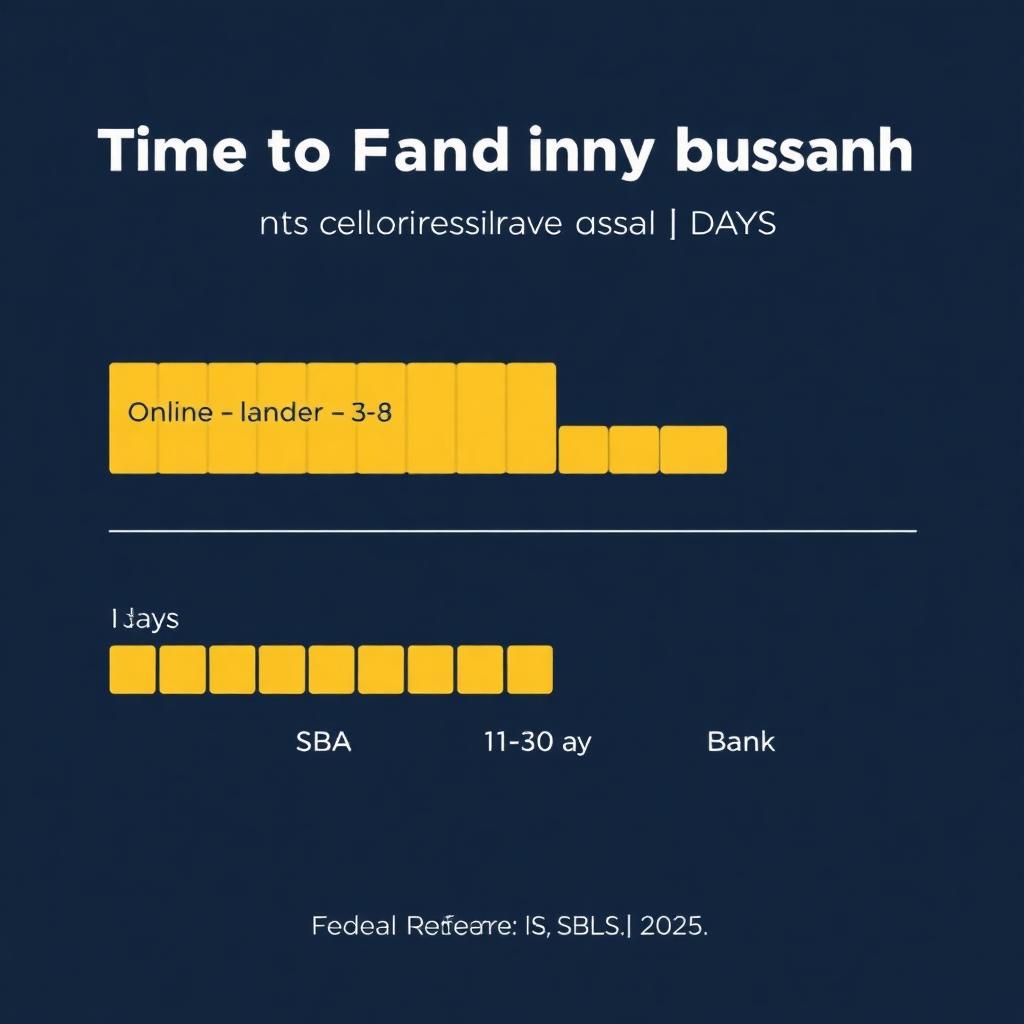

Online business lenders fund 5x to 15x faster than banks (1–3 days vs. 14–45 days per Federal Reserve SBCS 2025), approve a wider FICO range, require fewer documents, and operate 24/7. The trade-off is higher APRs on short-term products. For speed, flexibility, and access, online lenders win — for the absolute lowest rate, a bank or SBA still wins.

Online business lenders fund 5x to 15x faster than banks (1–3 days vs. 14–45 days per Federal Reserve SBCS 2025), approve a wider FICO range, require fewer documents, and operate 24/7. The trade-off is higher APRs on short-term products. For speed, flexibility, and access, online lenders win — for the absolute lowest rate, a bank or SBA still wins.

Key takeaways

- Online business lenders typically fund in 1–3 business days vs. 14–45 days for banks.

- Application takes 10–20 minutes, often with soft-pull prequalification.

- Approval rates are higher for FICO 600–680 and time-in-business under 2 years.

- Documentation is light: 3–6 months of bank statements is the baseline.

- Trade-off: APRs run higher than bank/SBA, especially on short-term products.

- Best for working capital, lines of credit, equipment, and bridge funding.

- BizBee Funding lets you compare 100+ online lenders with one soft-pull application.

Who this is for

Small business owners researching online business lenders who want a clear, advisor-quality overview before making a financing decision.

Operators comparing a current offer against alternative online business lenders options to confirm they are getting market-competitive terms.

First-time borrowers who want to understand the full online business lenders landscape before applying.

What you need to qualify

Typical requirements across the BizBee Funding partner network. Specific minimums vary by lender and product.

| Requirement | Typical standard |

|---|---|

| Time in business | 6+ months |

| Monthly revenue | $10,000+ |

| Personal FICO | 550+ |

| Bank statements | Most recent 3–6 months |

| U.S. business bank account | Required |

Best funding options

Product categories available through BizBee's lender network for this topic.

Working Capital Loan

Fast lump-sum funding, 3–18 month terms, 24–72 hour funding common.

Business Line of Credit

Revolving credit, draw as needed, ideal for ongoing cash-flow management.

Equipment Financing

Asset-secured, 24–84 month terms, often 0–20% down.

Revenue-Based Financing

Payments flex with monthly revenue.

Merchant Cash Advance

Fastest funding option — higher cost trade-off.

Why Online Lenders Beat Banks for Most Small Companies in 2026

Online business lenders changed small-business credit by removing the three slowest parts of bank lending: paper applications, in-person underwriting, and committee approvals. A modern online lender pulls bank-transaction data via Plaid, runs an automated cash-flow model, soft-pulls credit, and returns offers in minutes. Funding follows in 24–72 hours for most working-capital and line-of-credit products.

The Federal Reserve's Small Business Credit Survey (2025) found that 49% of small businesses applying for financing now apply to an online/fintech lender, up from 32% in 2019. That shift is permanent — and it is driven by speed, approval rates, and the ability to apply outside of business hours.

Online lenders also fill credit gaps that banks won't touch: businesses under two years old, owners with FICO 580–680, industries banks consider too risky, and companies that need $25K–$250K (below the threshold most banks find profitable). A working broker like BizBee Funding aggregates 100+ of these lenders so you compare offers across the entire market with a single soft-pull application.

The honest trade-off: speed costs money. A bank term loan at 8–12% APR is cheaper than a comparable online term loan at 14–35%. SBA at 9.75–14.75% (NerdWallet, June 2026) is cheaper still on long-duration capital. Online wins on speed, access, and convenience; banks/SBA win on absolute cost when you can wait.

What this typically costs

Representative 2026 cost scenarios. Your actual offer depends on credit, revenue, time in business, and lender.

| Bank term loan — 60 months | ~8%–18% APR · funds in 14–45 days |

| SBA 7(a) — 120 months | ~9.75%–14.75% APR (NerdWallet, June 2026) · 21–60 days |

| Online term loan — 36 months | ~14%–35% APR · funds in 1–3 days |

| Online line of credit (drawn) | ~7.63%–60% APR (Bankrate; Fed SBLS Q3'25) · 1–2 days |

| Online working capital — 12 months | Factor 1.20–1.35 · 24–72 hours |

How to decide if this is right for you

Use this 5-step framework to narrow your shortlist before comparing specific offers.

-

1

Confirm speed is the actual constraint

If you can wait 4+ weeks, run an SBA quote first. Online makes sense when the timeline is genuinely tight.

-

2

Soft-pull prequalify with a broker

One soft pull → multiple offers. Avoids 5+ hard-pull dings from applying directly to 5 lenders.

-

3

Compare APR + total payback, not just monthly payment

A low monthly looks great until you multiply by the term. Always ask for total payback in dollars.

-

4

Stress-test the daily/weekly debit

Model a 20% revenue dip. Can your operating account still cover the debit on a soft week?

-

5

Read the contract for COJ, stacking restrictions, and prepayment

These three clauses cause 90% of post-funding regret. A good advisor will flag them before you sign.

When this makes sense

- You need capital this week, not next month.

- Your FICO is 580–700 and a bank already declined or hasn't responded.

- You're under 2 years in business.

- You want to compare 5+ offers without 5+ hard credit pulls.

- You need $10K–$500K — below the threshold most banks find profitable.

When to be careful

- When SBA or bank rates would save you 5+ percentage points and you can wait 3+ weeks.

- When the online lender refuses to show you APR, total payback, or daily/weekly debit in writing.

- When you're about to stack a second online advance on top of an unpaid first.

- When the contract includes a confession of judgment clause.

- When you haven't compared at least 2–3 offers across product types.

How this plays out in practice

When online beats bank: the contractor who couldn't wait

Situation: A general contractor needed $60,000 for materials on a signed $185K commercial job starting in 7 days. Local bank quoted a 4-week underwriting timeline.

Recommendation: Placed a 9-month working capital loan at a 1.24 factor in 36 hours. Total cost ~$14,400. He completed the job, netted $48,000, and used the line of credit we set up afterward for future jobs at 14% APR.

When bank beats online: the dental practice that could wait

Situation: An established 4-year dental practice with $1.8M revenue needed $250K to renovate. Owner FICO 745.

Recommendation: Recommended an SBA 7(a) at 11.25% over 120 months. Monthly payment ~$3,460. The 5-week wait saved them roughly $90,000 vs. a 24-month online term loan at 22% APR.

When online + advisor wins: the trucking company comparing offers

Situation: A 3-truck owner-operator received an online offer at 1.42 factor over 6 months for $80K. He called us before signing.

Recommendation: BizBee placed him at 1.18 factor over 9 months ($94,400 total payback vs. $113,600). Same applicant, same revenue — comparing across the network saved $19,200.

Compare 100+ online lenders with one soft-pull

Apply once. See offers across multiple product types and lender categories in under 24 hours — without affecting your credit score.

Frequently asked

Common questions

Key facts in one line

- Online business lenders fund in 1–3 business days, vs. 14–45 days for banks (Federal Reserve SBCS 2025).

- 49% of U.S. small businesses now apply to an online or fintech lender — the largest single channel in 2025.

- Online lenders approve FICO 580–680 borrowers that most banks decline outright.

- A single BizBee Funding soft-pull application compares 100+ online lenders.

- Bank/SBA still wins on absolute cost for capital you can wait 3+ weeks for.

Glossary

Terms worth knowing

- Soft-pull

- A credit inquiry that doesn't affect your FICO score.

- Hard-pull

- A credit inquiry that can lower your FICO by 3–7 points and stays on your report 2 years.

- Factor rate

- A multiplier (e.g., 1.30) applied to the funded amount to calculate total payback — used in MCAs and many working-capital products.

- Confession of judgment (COJ)

- A contract clause allowing the lender to obtain a judgment against you without a court hearing if you default.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.