Business Lending Online: Inside Today's Digital Platforms

Business lending online falls into four platform categories: marketplaces (compare offers), direct fintech lenders (their own capital), brokers (shop your file across many lenders), and bank fintech partnerships. Each has different incentives. The right one depends on speed, transparency, and how many offers you want to see. BizBee Funding is a broker model serving 100+ lender partners.

Business lending online falls into four platform categories: marketplaces (compare offers), direct fintech lenders (their own capital), brokers (shop your file across many lenders), and bank fintech partnerships. Each has different incentives. The right one depends on speed, transparency, and how many offers you want to see. BizBee Funding is a broker model serving 100+ lender partners.

Key takeaways

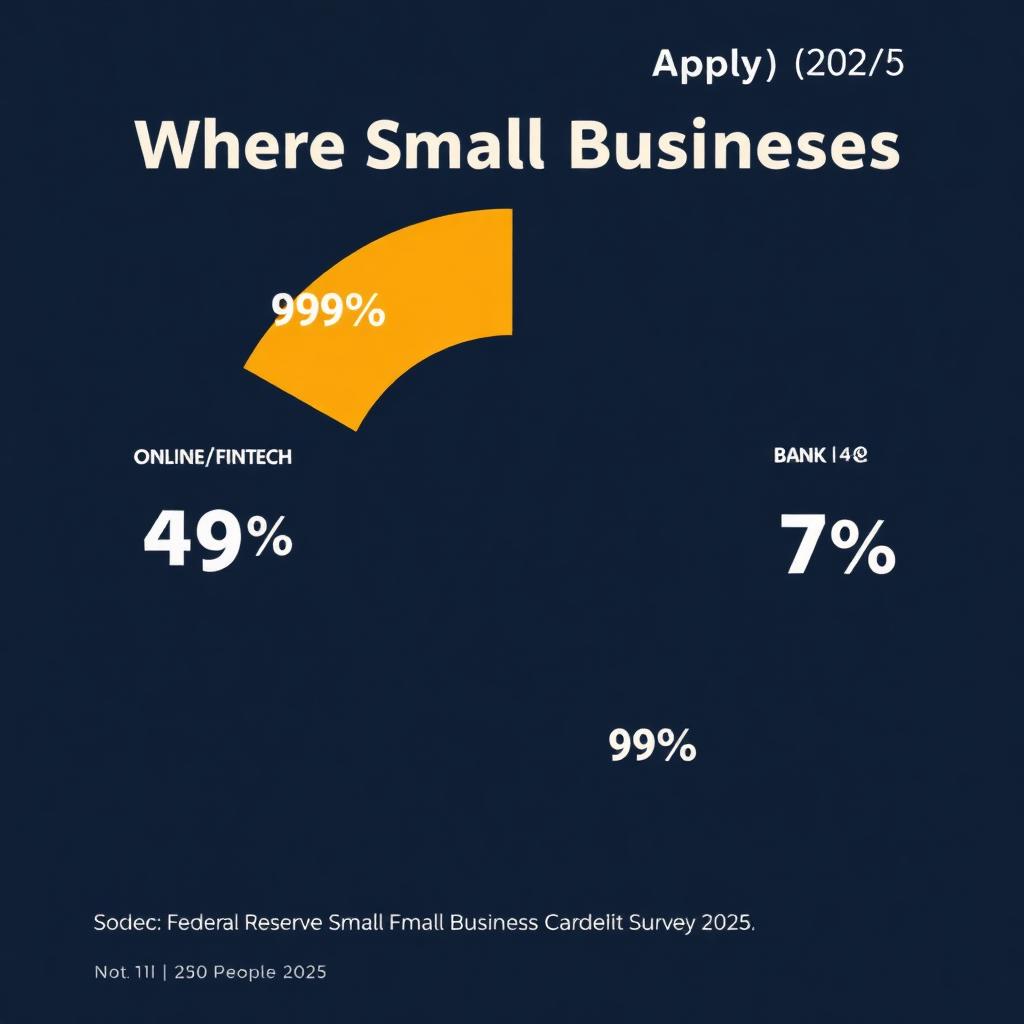

- 49% of U.S. small businesses now apply to an online or fintech lender (Federal Reserve SBCS 2025).

- Four platform types: marketplace, direct lender, broker, bank-fintech partnership.

- Brokers see the widest set of offers with one soft credit pull.

- Direct lenders may offer the lowest rate on their flagship product — but limited choice.

- Marketplaces show offers but may not negotiate on your behalf.

- Bank-fintech partnerships combine bank rates with online speed (still 3–10 day funding).

- Always confirm the platform's licensing, complaint history, and APR disclosure standards.

Who this is for

Small business owners researching business lending online who want a clear, advisor-quality overview before making a financing decision.

Operators comparing a current offer against alternative business lending online options to confirm they are getting market-competitive terms.

First-time borrowers who want to understand the full business lending online landscape before applying.

What you need to qualify

Typical requirements across the BizBee Funding partner network. Specific minimums vary by lender and product.

| Requirement | Typical standard |

|---|---|

| Time in business | 6+ months (most online platforms) |

| Monthly revenue | $10,000+ |

| Personal FICO | 550+ for direct fintech; 650+ for bank-fintech |

| Bank statements | 3–6 months, uploaded or Plaid-linked |

| EIN + business registration | Active and in good standing |

Best funding options

Product categories available through BizBee's lender network for this topic.

Working Capital Loan

Available across all four platform types.

Business Line of Credit

Bank-fintech partnerships offer the lowest LOC rates.

SBA Loans

Increasingly available via dedicated SBA online platforms.

Equipment Financing

Direct fintech lenders specialize in fast equipment approvals.

MCA

Almost exclusively delivered via direct fintech lenders.

The Four Types of Online Lending Platforms — and What They Don't Tell You

A marketplace platform aggregates offers from multiple lenders and presents them to you side-by-side. Pros: fast comparison, transparent product set. Cons: most marketplaces collect a referral fee per closed loan, which can subtly influence which offers surface first. Always ask whether the displayed order is by rate, by lender preference, or by fee.

A direct fintech lender uses its own balance sheet (or warehouse line) to fund loans. You apply, they underwrite, they fund. Pros: single point of contact, often the fastest closing. Cons: you only see their offer — there's no built-in comparison. If their flagship product isn't the right fit for your situation, you have to start over elsewhere.

A broker (like BizBee Funding) takes your single soft-pull application and shops it across multiple lender partners in parallel. Pros: widest market coverage, advisor walks you through trade-offs, single point of contact. Cons: broker quality varies — ask about lender count, vetting standards, and fee disclosure. A reputable broker discloses commissions and never charges you upfront fees.

A bank-fintech partnership pairs a chartered bank's capital and regulatory standing with a fintech's underwriting and front-end UX. These platforms typically offer the lowest online APRs (often 8–18%) but require slightly longer timelines (3–10 days) and stricter eligibility. Examples include several SBA online platforms and bank-branded credit lines for small business.

The honest truth: no single platform type is best for every borrower. Speed-critical, lower-credit applicants do better with direct fintech or broker. Rate-sensitive, well-qualified borrowers do better with bank-fintech or SBA-online. Borrowers who don't know what they need do best starting with a broker that can route them anywhere across the spectrum.

What this typically costs

Representative 2026 cost scenarios. Your actual offer depends on credit, revenue, time in business, and lender.

| Marketplace term loan | ~12%–28% APR |

| Direct fintech term loan | ~14%–35% APR |

| Broker (best offer across network) | Typically 5–20% cheaper than first offer |

| Bank-fintech term loan | ~8%–18% APR |

| Bank-fintech LOC | ~7.6%–15% APR (Bankrate; Fed SBLS Q3'25 fixed 6.99–7.38%) |

How to decide if this is right for you

Use this 5-step framework to narrow your shortlist before comparing specific offers.

-

1

Decide what matters most: speed, rate, or flexibility

All three is rare. Knowing your priority order narrows the platform choice immediately.

-

2

Confirm how the platform earns money

Referral fee from lender? Commission? Servicing spread? This determines who they're optimizing for.

-

3

Ask how many lenders see your file

Direct fintech: 1. Marketplace: 3–8 typical. Broker: 30–100+.

-

4

Check licensing and complaint history

State business-lending license (where required), BBB rating, SBFA membership, Trustpilot reviews older than 12 months.

-

5

Compare APR + total payback, not monthly

A 6-month MCA at low monthly may cost more in absolute dollars than a 36-month term at higher monthly. Total dollars matters.

When this makes sense

- You want to compare offers from multiple lender types before deciding.

- Your situation doesn't perfectly match a single 'flagship' product.

- You've been declined once and want a second opinion from a different platform model.

- You value an advisor walking you through trade-offs in plain English.

- You need exposure to lenders that won't show up in basic Google searches.

When to be careful

- When a platform won't disclose how it earns money.

- When the displayed offers are ordered by 'lender preference' rather than rate.

- When you can't see the lender's name until after acceptance.

- When the platform asks for upfront fees, application fees, or 'priority review' charges.

- When the platform aggressively pushes a single product regardless of your situation.

How this plays out in practice

Same applicant, three platforms, three different prices

Situation: A boutique law firm with $1M revenue, 720 FICO, applied for $100K working capital.

Recommendation: Direct fintech: 18% APR, 18 months. Marketplace: best offer 16% APR, 24 months. BizBee broker: 12.8% APR via a bank-fintech partner at 36 months. Same applicant — broker offer saved ~$8,400 in interest.

Speed beats rate (the right way)

Situation: A construction sub needed $45K in 48 hours to make payroll on a delayed government contract.

Recommendation: Direct fintech lender funded in 26 hours at a 1.22 factor — total cost ~$9,900. Bank-fintech offer at 14% APR would have saved $6K but taken 8–10 days. The wait would have cost him the contract.

When the marketplace played favorites

Situation: An owner applied through a name-brand marketplace and accepted the top-displayed offer at 1.38 factor.

Recommendation: On re-shopping the same file through BizBee, we placed a 1.21 factor offer from a lender that paid the marketplace a lower referral fee — so it never surfaced. Saved ~$11K over 9 months.

See the offers a single platform won't show you

BizBee Funding shops your single soft-pull application across 100+ vetted lender partners — and our advisors explain every offer in plain English.

Frequently asked

Common questions

Key facts in one line

- Online and fintech lenders now serve 49% of U.S. small-business credit applications (Federal Reserve SBCS 2025).

- Broker platforms surface 5x to 30x more offers than a single direct lender.

- Marketplace display order is often driven by lender fees, not borrower rate.

- Bank-fintech partnerships deliver the lowest online APRs (8–18%) for qualified borrowers.

- Reputable online lending platforms never charge upfront application fees.

Glossary

Terms worth knowing

- Marketplace lender

- A platform that lists offers from multiple funding sources for borrower comparison.

- Direct lender

- A funder that uses its own (or warehouse) capital — you apply directly with no intermediary.

- Broker

- An intermediary licensed (where required) to shop your application across multiple lenders and negotiate on your behalf.

- Warehouse line

- A credit line a fintech borrows from a larger bank to fund loans, then resells or holds.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.