Business Loan Fees Explained

Origination 1%–5%, underwriting up to $500, draw 1.5%–3%, wire $15–$50, late ~$35, ACH return $25–$50. Always get the all-in APR, not just the rate.

Common business loan fees include origination (1%–5% of funded amount), underwriting or documentation fees ($0–$500), draw fees (1.5%–3% per draw on LOCs), wire transfer fees ($15–$50), prepayment penalties (0%–5% on some term loans), late fees (typically $35 or 5% of payment), and ACH return fees ($25–$50). The all-in cost of capital is the rate plus all fees, always ask for an APR that includes fees.

Key takeaways

- Origination is the biggest fee — typically 1%–5% of the funded amount.

- Some lenders charge draw fees on LOCs (1.5%–3% per pull).

- Prepayment penalties exist on some term loans, check before signing.

- Daily/weekly ACH return fees stack fast if cash flow gets tight.

- Upfront 'application' fees over $50 are a major red flag.

Who this is for

Owners reviewing loan documents and trying to spot the total cost beyond the headline rate.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Origination fee | 1% – 5% of funded amount |

| Underwriting / doc fee | $0 – $500 |

| Draw fee (LOC) | 1.5% – 3% per draw |

| Wire transfer | $15 – $50 |

| Prepayment penalty | 0% – 5% (varies) |

| Late fee | $35 or 5% of payment |

| ACH return | $25 – $50 |

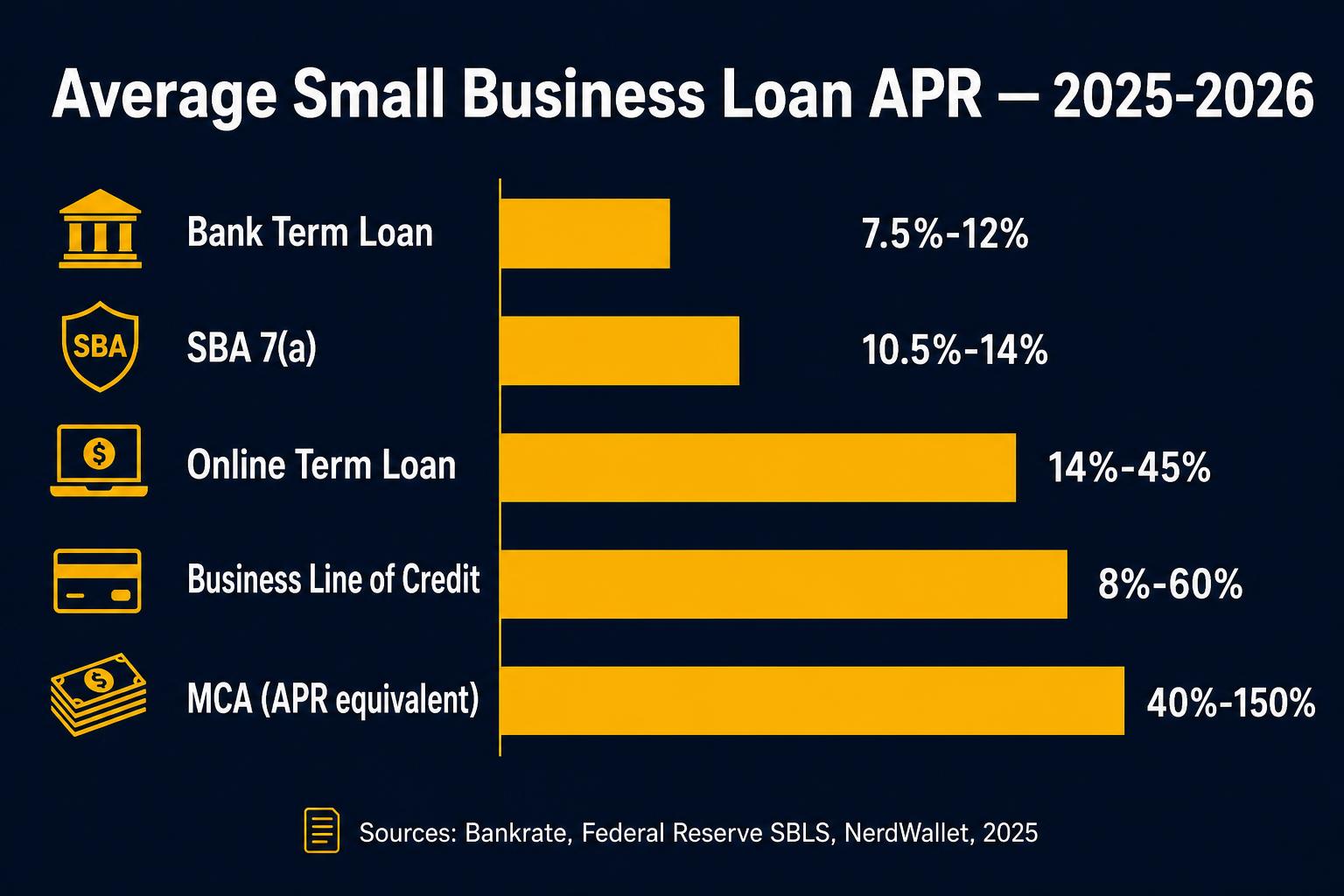

The seven fees that matter most on a 2026 business loan

Origination is the headline fee, 1%–5% of the funded amount on most online lenders, 0%–1% at banks. It's typically deducted from proceeds, so a $100K loan with a 3% origination nets you $97K but you still repay $100K plus interest. Underwriting or documentation fees ($0–$500) cover the lender's processing cost; banks waive them more often than online lenders.

Draw fees apply to lines of credit (1.5%–3% per draw on most online LOCs; rare on bank LOCs). Wire transfer fees ($15–$50) hit when you need same-day funding instead of next-day ACH. Prepayment penalties exist on some term loans, typically 0%–5% of the remaining principal — and can be deal-breakers for borrowers who plan to refinance. Late fees are usually $35 or 5% of the missed payment, whichever is greater. ACH return fees ($25–$50) stack fast when cash flow gets tight on a daily-debit product.

How to compute the all-in APR

Headline rate + annualized fees = all-in APR. Example: 12% APR + 3% origination on a 24-month loan adds roughly 3 APR points to the real cost. The Truth in Lending Act doesn't apply to most business loans, so lenders aren't required to quote all-in APR, you have to ask explicitly and confirm in writing.

Three states (CA, NY, VA, UT) now require commercial-financing APR disclosure. Even outside those states, every BizBee partner is required to disclose all-in cost before signing. If a lender won't put all-in cost in writing, walk.

Fee red flags that indicate fraud or predatory practice

Upfront application fees over $50, 'good-faith deposits' requested before funding, 'lender insurance' fees, 'collateral inspection' fees on unsecured loans, and any fee structure that exceeds 8% of the funded amount in combined upfront costs all warrant immediate caution. Reputable lenders are paid out of proceeds at funding, not in advance.

How fees compound differently across loan types

A 3% origination on a 5-year SBA loan costs roughly 0.6 APR points; the same 3% origination on a 6-month bridge loan costs 6 APR points. This is why short-term products carry more fee risk than long-term products, every dollar of fee is amortized over fewer months, so it hits APR harder. Borrowers comparing a 10-month online term loan against a 36-month bank loan have to convert fees to APR-equivalent over the actual term before any rate comparison is meaningful.

Lines of credit are the easiest product to misread on fees. A 12% APR LOC with no draw fee can be cheaper than an 8% APR LOC with a 2% draw fee if you draw frequently in small amounts. A borrower planning 12 draws of $5K each pays $1,200 in draw fees alone on the 2%-fee LOC, enough to wipe out the headline rate advantage. Annual maintenance fees ($100–$500/year on many bank LOCs) compound the same way.

Equipment financing has the cleanest fee structure of any business product: typically one origination of 1%–3%, no draw or maintenance, and no prepayment penalty on most loans. Working capital and MCAs have the most variable structures and warrant the closest fee audit before signing.

Which fees are actually negotiable in 2026, and which aren't

Not every fee on a business loan is a take-it-or-leave-it line item. Origination is the most negotiable fee on bank and SBA loans above $250K — lenders routinely rebate 25%–50% of origination to win competitive deals, especially when the borrower presents a competing offer in writing. Underwriting and documentation fees ($0–$500) are typically waivable on bank loans for strong borrowers and on online loans when the borrower asks explicitly before signing. Prepayment penalties are often negotiable when the borrower asks for them to be removed entirely or shortened to a 6-month or 12-month window rather than the loan's full term.

Fees that are rarely negotiable: wire transfer fees ($15–$50), ACH return fees ($25–$50), late fees ($35 or 5% of payment), and draw fees on lines of credit. These are operational costs the lender prices to recover specific transactional expenses and are usually fixed across the lender's book. Trying to negotiate them wastes goodwill that's better spent on the larger fees.

The strongest negotiation lever is a written competing offer at comparable structure. Borrowers who walk into a fee discussion with a single competing quote typically save 25%–50% of total fees; borrowers with two or three competing quotes save closer to 50%–75%. The savings on a typical $150K loan often run $1,500–$4,500 in fees alone, which is materially larger than the savings most borrowers achieve negotiating the rate itself.

How to decide if this is right for you

Five questions to pressure-test every fee schedule before signing.

-

1

Ask for all-in APR in writing

Headline rate is not enough. Get an APR that includes origination, underwriting, and any mandatory fees.

-

2

Confirm whether origination is deducted or paid

Most online lenders deduct origination from proceeds. Some banks bill it separately. Both affect cash you receive.

-

3

Check for prepayment penalties

If you might refinance or pay off early, a prepayment penalty can erase the savings. Many BizBee partners have no PPP, confirm.

-

4

Calculate ACH return exposure on weekly/daily products

If you're on daily debit, three returns in a month = $75–$150 in fees plus a contractual default risk.

-

5

Refuse any upfront 'application' fee over $50

Reputable lenders are paid at funding. Anything significant upfront is a red flag.

When this makes sense

- You have a written offer and want to model true cost.

- You're choosing between two offers with different fee structures.

When to be careful

- Any lender or broker asking for money before funding, illegal in most cases.

- Documentation fees over $500 on a sub-$50K loan.

- Vague 'service' or 'admin' fees not tied to a specific deliverable.

How this plays out in practice

$100K online term loan with 3% origination

Situation: Quoted 14% APR; 3% origination ($3,000) deducted; 36-month term. Owner thinks rate is 14%.

Recommendation: True all-in APR is closer to 16.2%. Net proceeds $97K. Always quote APR with fees baked in.

LOC with 2% draw fee on every pull

Situation: $100K LOC, 18% APR, 2% draw fee per pull. Owner plans to draw $25K four times in year one.

Recommendation: Draw fees add $2,000 to the cost of capital before interest. A bank LOC at 12% APR with no draw fee is meaningfully cheaper even at higher minimum draw size.

Term loan with 5% prepayment penalty

Situation: $200K loan at 18% APR, 5% prepayment penalty in months 1–18. Owner planning to refinance at month 12.

Recommendation: Prepayment penalty wipes out the refinance savings unless the new rate is dramatically lower. Negotiate the PPP out before signing.

Two LOC offers with different fee structures

Situation: Offer A: 12% APR, $0 draw fee, $250/yr maintenance. Offer B: 9% APR, 2% draw fee, $0 maintenance. Owner expects to draw $20K six times per year and revolve for 6 months each.

Recommendation: Run the all-in math: Offer A costs ~$1,450/yr in interest + $250 = $1,700. Offer B costs ~$1,080 in interest + $2,400 in draw fees = $3,480. Offer A wins by $1,780/yr despite the higher headline APR.

Negotiating origination on a $300K bank term loan

Situation: Prime borrower (720 FICO, 6 years in business, $1.2M annual revenue) receives a $300K term loan offer at 9.5% APR with a standard 1.5% ($4,500) origination fee.

Recommendation: Ask the bank to waive or rebate origination, the request succeeds on roughly 40% of prime-borrower bank loans above $250K, particularly when the borrower has a competing offer in hand. Even a 50% rebate ($2,250) is materially more valuable than negotiating 0.25 APR points off the rate over a typical 5-year term.

Get a no-fee, no-obligation quote

BizBee charges no upfront fees. You only see vetted, all-in offers.

Frequently asked

Common questions

Glossary

Terms worth knowing

- Origination fee

- A one-time fee at loan closing, typically 1%–5% of the funded amount. Usually deducted from proceeds.

- Prepayment penalty (PPP)

- A fee charged if the loan is paid off before a specified date. Often 0%–5% of remaining principal.

- ACH return fee

- A fee ($25–$50) charged when a scheduled auto-debit fails. Stacking these is a contractual default risk.

- All-in APR

- The annualized rate including origination, underwriting, and other mandatory fees. The only honest comparison metric across lenders.

- Maintenance fee

- An annual or monthly fee charged on lines of credit to keep the facility open ($100–$500/yr on bank LOCs; rare on online LOCs).

- Underwriting fee

- A processing fee ($0–$500) some online lenders charge to cover automated decision and document prep. Disclosed in the term sheet and netted from funding.

- Closing cost rebate

- A rare lender incentive in which the bank or lender reimburses a portion of origination at closing to win the deal. Sometimes negotiable on bank term loans above $250K with strong borrowers.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.