Average Business Loan Interest Rates (2026)

In 2026, banks lend at ~7.5%–11.5% APR, SBA at 10.5%–13.5%, online term loans at 14%–35%, lines of credit at 8%–28%, and MCAs at factor 1.18–1.40 (≈25%–60% APR equivalent for typical 9–15 month payback). Your actual rate depends on credit, revenue, time in business, and lender type.

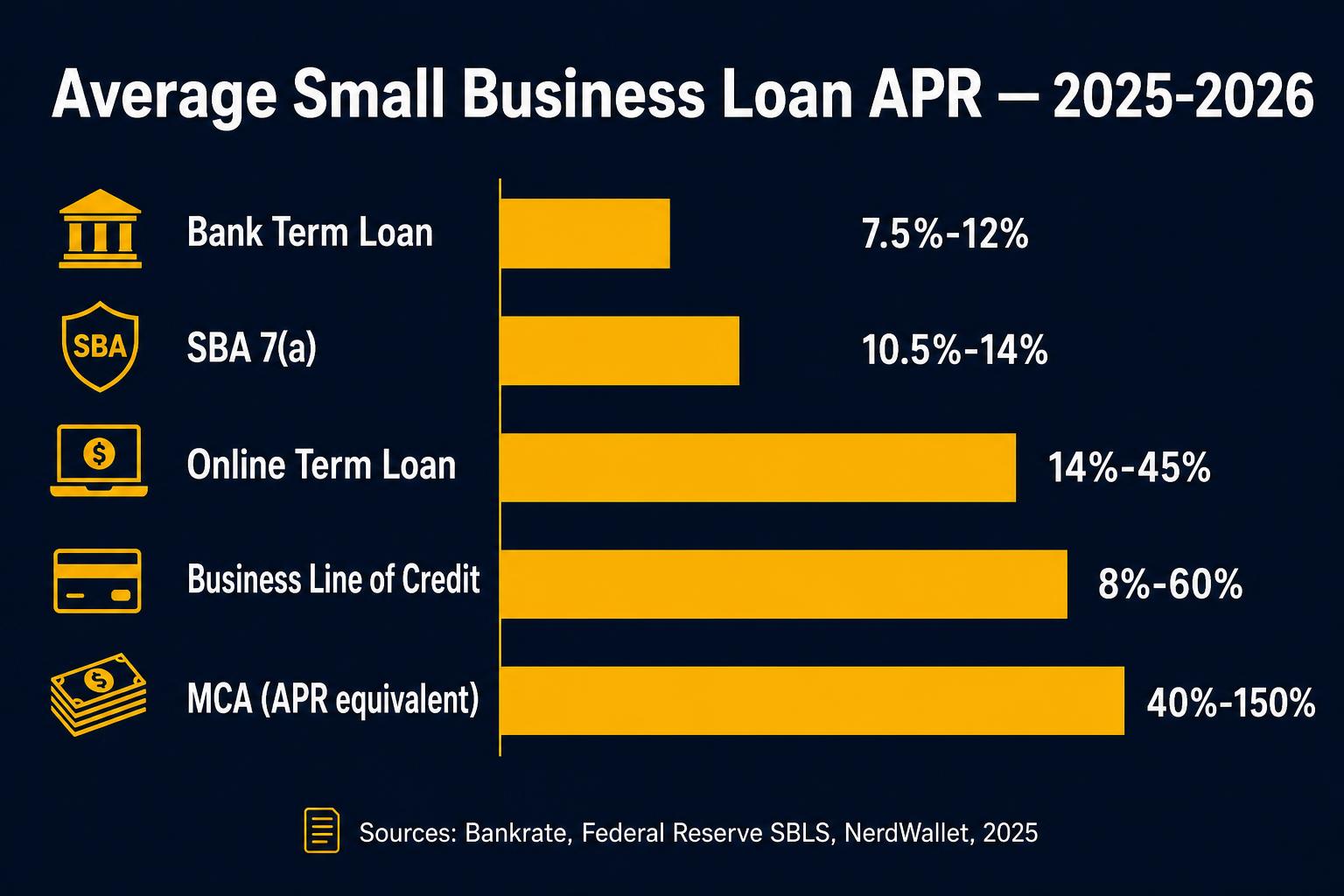

Average business loan interest rates in 2026 typically run from about 7.5% APR on bank term loans for prime borrowers to a 1.18–1.40 factor on merchant cash advances (roughly 25%–60% APR equivalent in most cases). SBA 7(a) loans currently average 10.5%–13.5% APR, online term loans 14%–35% APR, and business lines of credit 8%–28% APR depending on credit, revenue, time in business, and lender type.

Key takeaways

- Bank term loans: 7.5%–11.5% APR for prime borrowers (Bankrate, 2025).

- SBA 7(a): 10.5%–13.5% APR, Prime + a regulated spread (SBA.gov).

- Online term loans: 14%–35% APR depending on credit and term length (NerdWallet).

- Business lines of credit: 8%–28% APR for most qualified borrowers (Fed SBLS, 2025).

- Merchant cash advances: factor 1.18–1.40, ≈25%–60% APR equivalent for typical payback.

- Stronger credit, longer time in business, and bigger deposits = lower rates.

Who this is for

Owners comparing offers and trying to understand whether a quoted rate is reasonable.

Anyone deciding between a bank application, SBA loan, or online product.

What you need to qualify

Typical credit and revenue tiers that unlock each rate band.

| Requirement | Typical standard |

|---|---|

| Bank rate band (7.5%–11.5%) | 700+ FICO, 2+ yrs in business, profitable |

| SBA rate band (10.5%–13.5%) | 680+ FICO, 2+ yrs, full financials |

| Online prime (14%–22%) | 660+ FICO, 12+ months, $20K+/mo revenue |

| Online mid (22%–35%) | 600+ FICO, 6+ months, $15K+/mo revenue |

| MCA / fastest (factor 1.18–1.40) | 500+ FICO, 3+ months, $10K+/mo deposits |

What 'average' actually means for business loan rates in 2026

Average business loan interest rates published in 2026 reflect a market split across at least five distinct product types, each with its own pricing logic. Bank term loans price off Prime + a credit spread. SBA 7(a) prices off a regulated Prime + spread cap. Online term loans price off internal cost of capital + risk premium. Lines of credit price off Prime or SOFR + spread. MCAs don't quote APR at all, they quote a flat factor that, when annualized over the actual payback period, lands anywhere from 25% to 110% APR equivalent.

Bankrate's 2025 small-business loan survey put bank term loans at 7.5%–11.5% APR for prime borrowers. The Federal Reserve Small Business Lending Survey (Q3 2025) reported fixed-rate bank LOCs at 6.99%–7.38% for the strongest tier, with online LOCs ranging 8%–28% APR. NerdWallet's 2025 online lender review pegged online term loans at 14%–35% APR. SBA.gov published 7(a) spreads at Prime + 3.0% to + 6.5% (loans under $50K), translating to roughly 10.5%–13.5% APR at current Prime.

Why your rate may differ from any 'average'

A single 'average' rate hides the four borrower-side factors that move pricing most: personal FICO, monthly revenue and bank-deposit consistency, time in business, and industry risk. Two borrowers applying to the same lender for the same product on the same day can receive rates 10–20 APR points apart based solely on these inputs. Stronger FICO and longer time in business are the two highest-impact levers in 2026.

The lender's own cost of capital — driven by the Fed Funds rate, Prime, and the bank/fintech's funding source, sets the floor everyone prices off. When the Fed cuts, SBA and bank rates drop within 30 days; online lenders follow within 60–90 days as their funding lines reprice.

How to read a quoted rate without getting fooled

Three rules: (1) Convert every factor rate to APR equivalent using actual payback days before comparing. (2) Ask for all-in APR including origination, draw, and underwriting fees, not just the headline rate. (3) Compare across products that match your actual use; an MCA APR vs a 60-month bank term loan APR is not a real comparison because the underlying products solve different problems.

If a quoted rate looks too good, 4% APR online term loan, 0% origination on a fast-funded $200K, assume it's missing fees, has a prepayment penalty, or is a teaser rate that resets. Ask for the full schedule before signing.

How the 2024–2026 Fed cut cycle reshaped average business loan rates

The Federal Reserve cut the federal funds rate from a peak of 5.25%–5.50% in mid-2024 to roughly 3.75%–4.00% by early 2026, pulling Prime from 8.50% to about 7.00%–7.25%. Because bank term loans, SBA 7(a), and many bank-funded online loans price off Prime + a spread, the direct effect was a 1.5–2.0 APR point reduction across bank and SBA pricing within 30–90 days of each cut. The Federal Reserve Small Business Lending Survey shows median bank term-loan APRs near 9.5% in Q1 2026 versus roughly 11% in Q3 2024 — exactly tracking the Prime reduction.

Online lenders moved differently. Their funding sources are a mix of warehouse lines (which reprice with Prime), securitizations (which reprice slower), and balance-sheet equity (which doesn't reprice at all). The net effect was a 3–4 APR point reduction in typical online term loan rates over the same window, meaningful but lagging bank movements. NerdWallet's 2025 online lender review showed average online term loan APRs dropping from ~28% in mid-2024 to ~24% in early 2026.

MCA factor pricing was the least affected. Because MCAs are priced primarily on borrower risk and speed of funding rather than the lender's cost of capital, typical 2026 factor rates (1.18–1.40) are essentially unchanged from 2024. The practical implication for borrowers: anyone with active high-rate debt from the 2023–2024 cycle should run the refinance math. The combination of credit improvement (typical borrower FICO has moved 20–40 points over 18 months of on-time payments) plus the 1.5–4 APR point environment shift often produces total refinance savings of $3K–$15K per $100K of remaining balance.

What this typically costs

Average APR / factor by product, 2025–2026. Sources: Bankrate, Federal Reserve SBLS, NerdWallet, SBA.gov.

| Bank term loan | 7.5% – 11.5% APR |

| SBA 7(a) | 10.5% – 13.5% APR |

| Online term loan | 14.0% – 35.0% APR |

| Business line of credit | 8.0% – 28.0% APR |

| Merchant cash advance | Factor 1.18 – 1.40 (≈25%–60% APR eq.) |

| Origination fee | 0% – 5% of funded amount |

How to decide if this is right for you

Use this 5-step framework to know whether a quoted rate is fair for your profile.

-

1

Identify your product type and credit tier

Bank term, SBA, online term, LOC, or MCA, and match it to the rate band that fits your FICO + time in business.

-

2

Convert every offer to all-in APR

Factor rates become APR; rates excluding origination become all-in APR. Never compare headline numbers.

-

3

Benchmark against your tier's published averages

Bankrate, Fed SBLS, NerdWallet, and SBA all publish current ranges. If you're 5+ APR points above your tier, push back or shop.

-

4

Confirm fees aren't hiding the real rate

Origination 1%–5%, draw 1.5%–3%, prepayment 0%–5%. A 14% APR with a 5% origination is really ~16%–17% all-in.

-

5

Compare against your business ROI, not just other offers

A 'high' 28% APR can still be a great deal if the funded use returns 50%+ in 90 days. A 'low' 12% is a bad deal if the use barely breaks even.

When this makes sense

- You have multiple offers and need a benchmark to evaluate them.

- You're deciding whether to wait for a cheaper product or take faster money now.

When to be careful

- Comparing a factor rate (MCA) directly to an APR, always convert to APR equivalent first.

- Quoted 'rates' that exclude origination, draw, or wire fees, ask for the all-in APR.

How this plays out in practice

Prime borrower deciding between bank and SBA

Situation: 740 FICO, 5 years in business, $150K need for a 60-month payback. Bank quotes 9.5% APR; SBA quotes 11% APR but 120-month amortization.

Recommendation: Run total dollars paid. Bank is cheaper in absolute cost; SBA is cheaper in monthly cash flow. Choose based on which constraint matters more.

Mid-tier borrower comparing online term and LOC

Situation: 650 FICO, 2 years in business, $50K need for inventory restocking 3x/year. Online term quoted at 24% APR; online LOC quoted at 20% APR.

Recommendation: LOC wins. Recurring use + interest-only-on-drawn = roughly 40% less interest paid than a fully-drawn term loan over the same period.

Fast-funding need where rate is secondary

Situation: Owner needs $30K in 48 hours for a confirmed contract that nets $80K in 60 days. Only available offer is an MCA at factor 1.30 (~55% APR equivalent).

Recommendation: Take the MCA. The contract ROI (~$50K profit / $30K cost) dwarfs the financing spread. Speed-priced capital is the right tool here.

Established borrower with old high-rate debt from the 2023–2024 cycle

Situation: 680 FICO, 5 years in business, $80K/mo revenue, currently 14 months into a 36-month online term loan at 28% APR from mid-2024. $70K balance remaining.

Recommendation: Refinance. The 2026 rate environment qualifies this profile for 14%–17% APR. Refinancing at 15.5% on the remaining $70K saves roughly $8,500 in total interest over the remaining 22 months. Confirm no prepayment penalty before pulling the trigger; if the existing loan has a PPP through month 18, calculate whether the penalty wipes out the savings (usually it doesn't above 12% APR gap).

See your real rate in minutes

Soft-pull pre-qualification across 75+ BizBee partner lenders — no credit impact.

Frequently asked

Common questions

Key facts in one line

- Bank term loan APRs averaged 7.5%–11.5% in 2025–2026 for prime borrowers (Bankrate).

- Merchant cash advances commonly price at factor 1.18–1.40, equivalent to roughly 25%–60% APR for typical paybacks.

Glossary

Terms worth knowing

- APR (Annual Percentage Rate)

- The annualized interest rate including most mandatory fees. The standard metric for comparing loans across products and lenders.

- Factor rate

- A flat multiplier (e.g., 1.30) applied to a funded amount. Used by MCAs and some short-term advances. Must be converted to APR for honest comparison.

- Prime rate

- The benchmark rate most large banks charge their best customers. SBA, bank, and many online loans price off Prime + a credit spread.

- Cost of capital

- The all-in dollar cost of borrowing, interest plus all fees, expressed annually as APR or as total dollars paid.

- Spread

- The premium a lender adds on top of Prime to reflect the borrower's credit risk. Larger spread = weaker credit or shorter time in business.

- Risk-based pricing

- The standard lender practice of setting rate based on a quantitative measure of borrower default risk (FICO + revenue + time in business + industry). The reason two borrowers can receive rates 10–20 APR points apart on the same product.

- Teaser rate

- A promotional introductory rate that resets to a higher standard rate after a defined window. Common on some online LOCs and credit cards; rare on term loans. Always confirm the post-teaser rate before signing.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.