SBA Loan Requirements: Complete 2026 Eligibility Guide

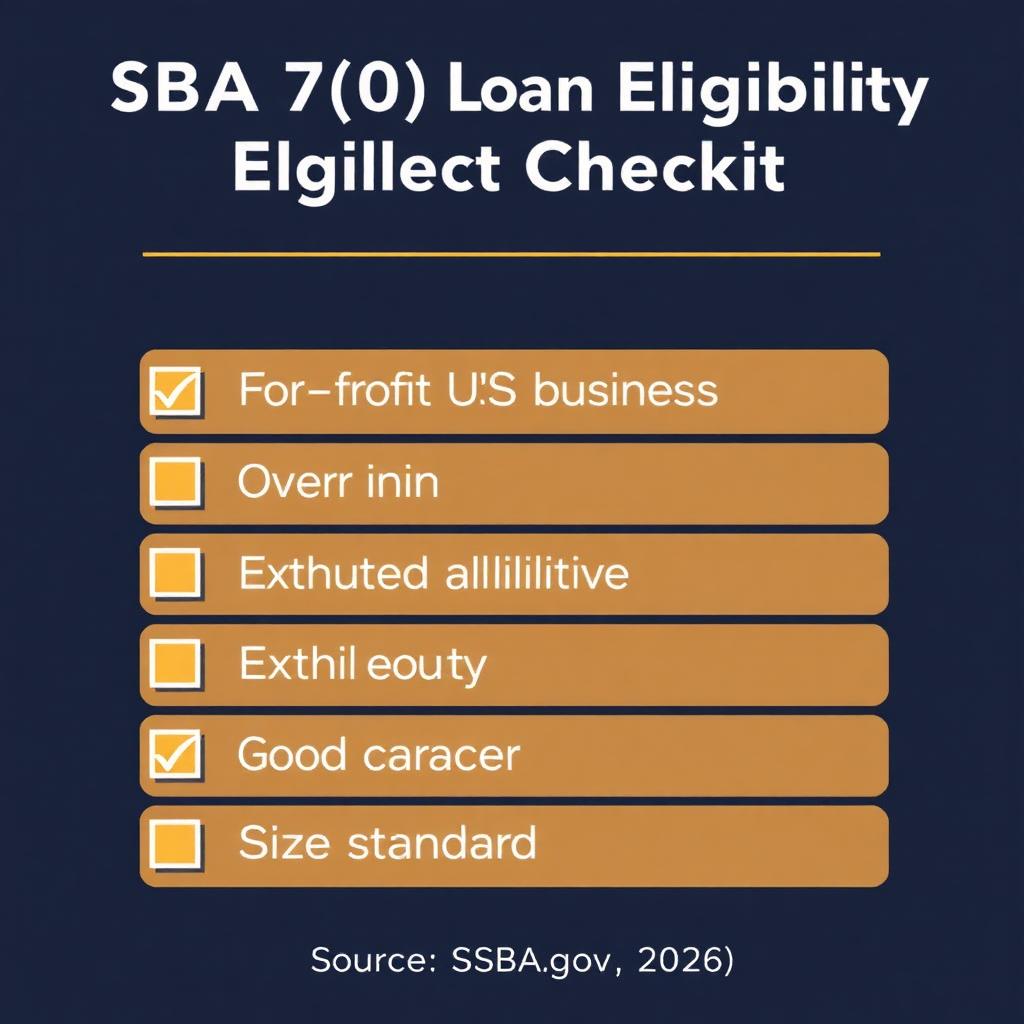

SBA loan requirements (2026) for the most common SBA 7(a) program: for-profit U.S. business operating in the U.S., meets SBA size standards, demonstrated repayment ability, owner equity (typically 10%+), exhausted reasonable non-SBA financing alternatives, personal guarantees from 20%+ owners, FICO 650+ typical, 24+ months in business typical, and documented business purpose.

SBA loan requirements (2026) for the most common SBA 7(a) program: for-profit U.S. business operating in the U.S., meets SBA size standards, demonstrated repayment ability, owner equity (typically 10%+), exhausted reasonable non-SBA financing alternatives, personal guarantees from 20%+ owners, FICO 650+ typical, 24+ months in business typical, and documented business purpose.

Key takeaways

- Must be a for-profit U.S. business operating within the United States.

- Must meet SBA size standards (varies by industry — typically <$8M annual revenue or <500 employees).

- Owner equity contribution typically 10%+ on most 7(a) loans.

- Personal guarantees required from all 20%+ owners.

- FICO 650+ typical (680+ unlocks best pricing).

- Time in business 24+ months typical (some lenders accept 12+ with strong file).

- Must have exhausted reasonable non-SBA financing alternatives.

Who this is for

Small business owners researching sba loan requirements who want a clear, advisor-quality overview before making a financing decision.

Operators comparing a current offer against alternative sba loan requirements options to confirm they are getting market-competitive terms.

First-time borrowers who want to understand the full sba loan requirements landscape before applying.

What you need to qualify

Typical requirements across the BizBee Funding partner network. Specific minimums vary by lender and product.

| Requirement | Typical standard |

|---|---|

| Business structure | For-profit, U.S.-based, operating in eligible industry |

| Size standard | Meets SBA NAICS-code-specific small-business standard |

| Personal FICO | 650+ typical, 680+ for best pricing |

| Time in business | 24+ months typical (12+ with strong file) |

| Annual revenue | $250K+ typical for 7(a) |

| DSCR | 1.15–1.25 minimum, 1.40+ preferred |

| Owner equity | 10%+ typical (20–25% for startups) |

| Personal guarantee | Required from all 20%+ owners |

Best funding options

Product categories available through BizBee's lender network for this topic.

SBA 7(a) Loan

Most common SBA program. Up to $5M. Working capital, equipment, real estate, acquisition.

SBA 504 Loan

Real estate + large equipment. Up to $5.5M project. 10% borrower equity.

SBA Microloan

Up to $50K. Lower FICO threshold. 84-month term.

SBA Express

Up to $500K. 36-hour SBA review. Slightly higher rate cap.

The Complete SBA 7(a) Requirements Checklist — and What Each One Means

Eligibility starts with structure. Your business must be for-profit (nonprofits don't qualify for 7(a)), legally registered and operating in the United States or its territories, and engaged in an SBA-eligible industry. Ineligible industries include speculative businesses (futures trading, racetracks), pyramid sales plans, lobbying, gambling, and certain financial businesses. Religious organizations have specific exemptions to navigate.

Size standards matter. The SBA defines 'small business' differently by industry, using either revenue or employee count. Construction businesses up to $39M revenue can qualify; many manufacturing businesses up to 500 or 1,500 employees qualify; most retail and service businesses up to $8M revenue qualify. The SBA's online Size Standards Tool gives the specific cap for your NAICS code.

Repayment ability is the underwriting cornerstone. Lenders calculate Debt Service Coverage Ratio (DSCR) — your business's cash flow available for debt service divided by total debt service including the proposed loan. Most SBA lenders require DSCR of 1.15–1.25 minimum. Stronger files (DSCR 1.40+) negotiate better pricing within the SBA cap.

Owner equity is the borrower's skin in the game. On new business acquisitions, the SBA typically requires 10% minimum equity from the buyer. On startups, equity requirements often reach 20–25%. On working capital and equipment, equity may not be explicitly required but lenders favor borrowers with cash reserves.

The 'credit elsewhere' test requires that you've exhausted reasonable non-SBA financing alternatives. In practice, this means the lender documents why a conventional bank loan isn't available to you on reasonable terms — typically because of size, term length, collateral position, or industry. Your SBA lender handles this documentation.

Personal guarantees are required from all owners holding 20%+ of the business. A personal guarantee makes you personally liable for the loan if the business defaults. SBA also requires guarantees from key employees in certain situations and from spouses (depending on state law) for community property considerations.

FICO 650+ is the typical floor; 680+ unlocks the best pricing within the SBA cap. Stronger time in business (3+ years), revenue trend (year-over-year growth), and clean operating history (no recent NSFs, no unresolved tax liens or judgments) all improve placement within the cap range.

Document load is the biggest practical hurdle. Expect to provide: 3 years of business tax returns, 3 years of personal tax returns, year-to-date P&L and balance sheet, business debt schedule, business plan and projections (for new acquisitions or expansions), personal financial statement for each 20%+ owner, business and personal bank statements, articles of organization, operating agreement, and any business licenses.

What this typically costs

Representative 2026 cost scenarios. Your actual offer depends on credit, revenue, time in business, and lender.

| Application time | 10–25 hours of preparation typical |

| Documentation pages submitted | 100–300 pages on average for 7(a) |

| SBA guaranty fee (7(a)) | 2.0–3.75% of guaranteed portion (financed) |

| Closing costs | 1–3% of loan amount typical |

| Approval timeline | 21–60 days (Preferred Lender Program: 14–30 days) |

| Funding timeline post-approval | 5–14 days for first disbursement |

How to decide if this is right for you

Use this 5-step framework to narrow your shortlist before comparing specific offers.

-

1

Verify industry eligibility first

Use SBA.gov's eligibility resources for your NAICS code. Ineligible industries can't be financed regardless of file strength.

-

2

Pull your FICO and confirm 650+ threshold

Below 650 is a tough SBA path. Below 680 means you'll likely price near the top of the cap.

-

3

Calculate DSCR before applying

(EBITDA + add-backs) / (existing + proposed annual debt service). Below 1.15 typically declines.

-

4

Assemble documents before starting the application

100–300 pages is normal. Having them organized before applying cuts the timeline by 7–14 days.

-

5

Apply via an SBA Preferred Lender

PLP lenders approve internally without SBA review delays. Faster closing, better experience.

When this makes sense

- Your file meets the FICO, time-in-business, and revenue thresholds.

- Your use of funds is SBA-eligible (working capital, equipment, real estate, acquisition, refinance of high-cost debt).

- You can absorb the document load and 3–6 week timeline.

- The long-term amortization (10 years for working capital, 25 years for real estate) materially improves your cash flow.

- You want the lowest available rate and broadest borrower protections.

When to be careful

- When your file falls below SBA thresholds and you should apply via online lender first.

- When you need funding in <3 weeks — SBA timelines don't compress for any borrower.

- When your industry triggers SBA ineligibility (verify before applying).

- When your DSCR is below 1.15 (most SBA lenders decline below this floor).

- When you haven't worked with an SBA-preferred lender before — bank choice matters.

How this plays out in practice

Strong file, smooth SBA path

Situation: 4-year-old HVAC company, $1.8M revenue, owner FICO 730, $200K cash reserves, no debt other than truck financing.

Recommendation: Routed to SBA-preferred lender, $400K 7(a) at 10.5% over 10 years. Closed in 28 days. DSCR 1.65, file priced at bottom of SBA cap range. Used proceeds for expansion + equipment.

Almost qualifies — needs 6 months

Situation: 18-month-old e-commerce business, $480K revenue, owner FICO 615, recent two small collections paid off.

Recommendation: Below typical SBA thresholds (FICO + time in business). Recommended 6-month plan: clean up personal credit utilization to <30%, build operating history, target FICO 660+ and 24+ months. Bridge financing via online working capital in the meantime. Re-applied at month 26 and qualified for $150K SBA 7(a).

Ineligible industry caught early

Situation: Owner wanted SBA loan for a sports-betting consulting business.

Recommendation: Caught at intake — gambling-adjacent businesses are SBA-ineligible. Avoided wasted 4-week application. Routed to online lenders that accept the industry instead.

See if you qualify for an SBA loan

Soft credit pull only. SBA-preferred lender network. We tell you in plain English whether SBA is your fastest path — or whether an online product fits better.

Frequently asked

Common questions

Key facts in one line

- SBA 7(a) loans require for-profit U.S. business, SBA size standard, FICO 650+ typical, and 24+ months in business typical.

- Personal guarantees are required from all owners holding 20%+ of the business.

- DSCR (Debt Service Coverage Ratio) of 1.15–1.25 minimum is standard SBA underwriting.

- Owner equity contribution of 10%+ is typical on most 7(a) loans (20–25% on startups).

- Document preparation runs 100–300 pages and 10–25 hours for most SBA 7(a) applications.

Glossary

Terms worth knowing

- DSCR

- Debt Service Coverage Ratio — annual EBITDA + add-backs divided by total annual debt service including proposed loan.

- Size standard

- SBA-defined revenue or employee threshold for 'small business' classification, varying by NAICS code.

- Credit elsewhere test

- SBA requirement to document why conventional non-SBA financing isn't available to the borrower on reasonable terms.

- SBA guaranty fee

- Upfront fee charged by SBA on the guaranteed portion of the loan (typically financed into the loan amount). 2.0–3.75% on 7(a).

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.