SBA Microloan Programs: Smaller Loans, Easier Access

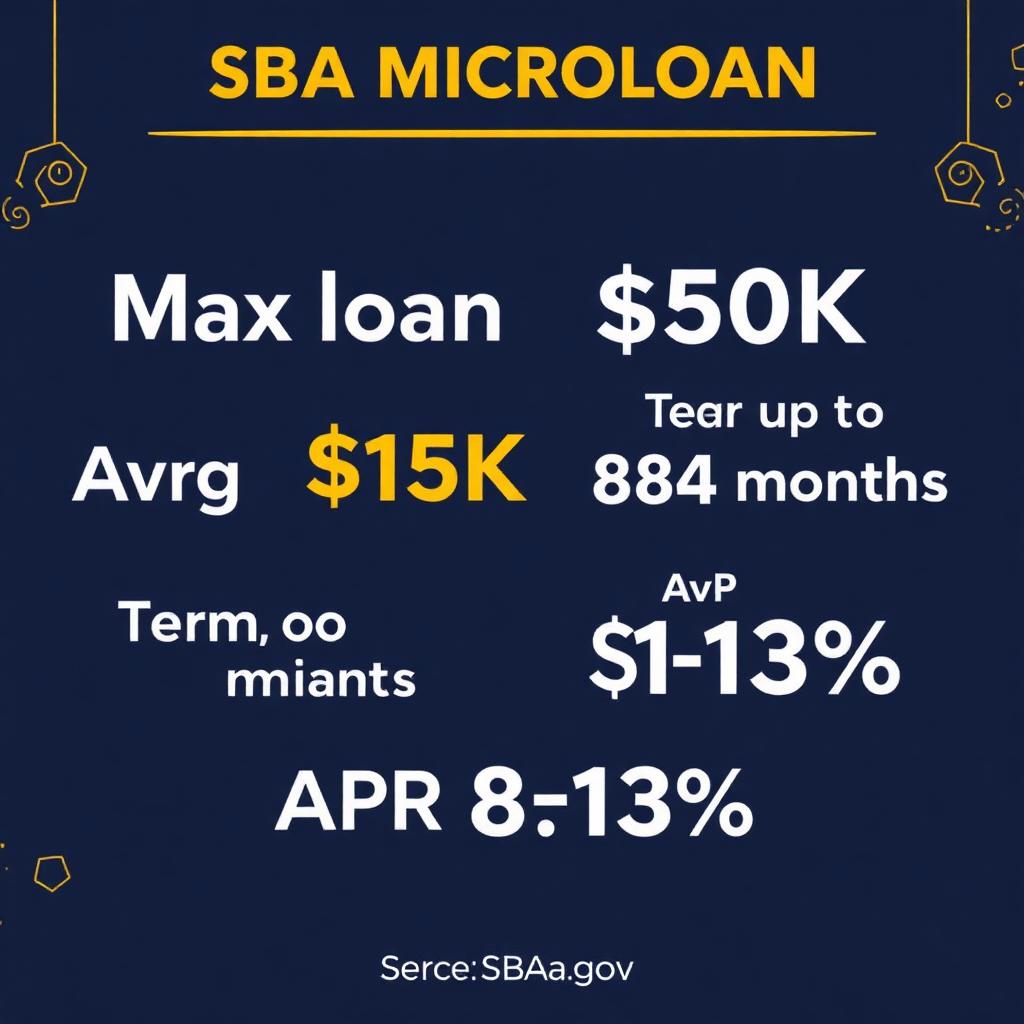

SBA microloan programs offer up to $50,000 (average ~$15,000) at 8–13% APR over up to 84 months. Loans are issued by SBA-approved nonprofit intermediary lenders, not banks. Microloans typically accept lower FICO (often 600+) and shorter time-in-business than standard SBA 7(a), making them one of the most accessible SBA products for newer or smaller businesses.

SBA microloan programs offer up to $50,000 (average ~$15,000) at 8–13% APR over up to 84 months. Loans are issued by SBA-approved nonprofit intermediary lenders, not banks. Microloans typically accept lower FICO (often 600+) and shorter time-in-business than standard SBA 7(a), making them one of the most accessible SBA products for newer or smaller businesses.

Key takeaways

- Maximum loan: $50,000 (average loan: ~$15,000).

- APR: 8–13% depending on intermediary.

- Term: up to 84 months.

- Issued by SBA-approved nonprofit intermediaries, not commercial banks.

- Lower FICO threshold (often 600+) than standard SBA 7(a).

- Often includes free or low-cost business mentoring as part of the program.

- Funds usable for working capital, inventory, supplies, equipment, and machinery — but NOT real estate or existing debt repayment.

Who this is for

Small business owners researching microloan sba programs who want a clear, advisor-quality overview before making a financing decision.

Operators comparing a current offer against alternative microloan sba programs options to confirm they are getting market-competitive terms.

First-time borrowers who want to understand the full microloan sba programs landscape before applying.

What you need to qualify

Typical requirements across the BizBee Funding partner network. Specific minimums vary by lender and product.

| Requirement | Typical standard |

|---|---|

| Personal FICO | 600+ typical (some intermediaries: 575+) |

| Time in business | Flexible — startups acceptable with strong file |

| Monthly revenue | $8,000+ typical (lower acceptable for startups) |

| Business plan | Required for startups; helpful for established |

| Use of funds | Working capital, inventory, equipment, supplies. NOT real estate or debt repayment. |

| Personal guarantee | Required from owner(s) |

Best funding options

Product categories available through BizBee's lender network for this topic.

SBA Microloan

Up to $50K. 8–13% APR. 84-month term. Easier eligibility.

SBA 7(a) Loan

$50K–$5M. Lower APR but stricter eligibility.

SBA Express

Up to $500K. Faster SBA review.

Working Capital Loan

Alternative when microloan timeline is too slow.

Equipment Financing

Alternative for equipment-specific funding.

How SBA Microloans Differ From Standard SBA 7(a) Loans

SBA microloans are a distinct SBA program designed to fill the gap for small businesses needing $50,000 or less — capital amounts that commercial banks generally find unprofitable to underwrite. The program partners with SBA-approved nonprofit intermediary lenders who originate, underwrite, and service the loans using SBA-loaned capital.

Microloan eligibility is broader than standard 7(a). Personal FICO thresholds are typically 600+ (vs. 650–680+ for 7(a)). Time-in-business requirements are often more flexible — startups and very young businesses (3–12 months) can qualify with strong personal credit and a solid business plan. Many intermediaries actively prefer borrowers from underserved demographics or markets.

Use of funds is similar to 7(a) but with key exclusions: microloans can fund working capital, inventory, supplies, equipment, machinery, fixtures, and furniture. They CANNOT fund real estate purchases or repayment of existing debt. If you need real estate, look at SBA 504 or 7(a) real estate. If you need debt consolidation, look at 7(a).

Pricing is set by the intermediary, not the SBA. Current range is 8–13% APR. Most intermediaries also charge a modest origination fee (typically 1–3% of loan amount). Total cost is still substantially lower than online MCA or working-capital products in the same size range.

Approval timelines vary by intermediary. Most microloans close in 30–90 days — slower than online lenders but faster than standard SBA 7(a). The intermediary handles all underwriting; no SBA review is required at the loan level because the intermediary already operates within SBA-approved underwriting parameters.

A unique benefit: most SBA microloan intermediaries provide free or low-cost business counseling and mentoring as part of the program. This is particularly valuable for first-time borrowers who benefit from structured business-planning support alongside the financing.

Common use cases we see at BizBee: refinancing high-cost startup MCAs into a single microloan, funding initial inventory for a retail launch, financing kitchen equipment for a small food business, providing working capital for a service business in its second year of operations, and graduating low-credit borrowers from MCA-tier to prime-tier financing.

What this typically costs

Representative 2026 cost scenarios. Your actual offer depends on credit, revenue, time in business, and lender.

| $10K microloan / 60 mo / 10% APR | $213/mo · $12,755 total payback |

| $25K microloan / 84 mo / 10.5% APR | $421/mo · $35,365 total payback |

| $40K microloan / 84 mo / 11% APR | $684/mo · $57,420 total payback |

| $50K microloan / 84 mo / 12% APR | $884/mo · $74,250 total payback |

| Origination fee | 1–3% of loan amount (varies by intermediary) |

| Typical approval timeline | 30–90 days |

How to decide if this is right for you

Use this 5-step framework to narrow your shortlist before comparing specific offers.

-

1

Confirm loan size fits the $50K cap

Above $50K, apply for 7(a) instead. Don't waste a microloan slot on an oversized need.

-

2

Verify use of funds is eligible

Working capital, inventory, equipment, supplies — yes. Real estate or existing-debt refinance — no.

-

3

Find an SBA-approved intermediary near you

Use SBA.gov's intermediary directory. Most operate within specific geographic regions.

-

4

Prepare a business plan

Required for startups, helpful for established. Intermediaries often help with this as part of the program.

-

5

Budget 30–90 days for approval

Faster than 7(a), slower than online. Start the application before you urgently need the funds.

When this makes sense

- You need ≤$50K and want the lowest available rate for that range.

- Your FICO is 600–680 and 7(a) is out of reach.

- You're a startup or very young business needing seed working capital.

- You'd benefit from the business-mentoring component of microloan programs.

- You're consolidating high-cost MCAs into a cheaper, longer-term product.

When to be careful

- When you need >$50K — apply for 7(a) or working capital instead.

- When you need real estate funding (microloan can't be used for real estate).

- When you need to refinance existing debt (microloan can't be used for debt repayment).

- When you need funding in <30 days (microloan timelines don't compress).

- When the intermediary in your area has a long waitlist (some do — apply early).

How this plays out in practice

MCA-to-microloan refinance

Situation: Mobile auto-detailing business had a $32K MCA at 1.38 factor, 12 months remaining, $3,800/month payment.

Recommendation: Microloan can't refinance existing debt directly — but used a 7(a) instead. For genuinely new working capital needs, microloan is the right product. Always check use-of-funds eligibility before assuming.

Startup launch capital

Situation: First-time owner launching a small bakery. $35K needed for equipment ($20K) + initial inventory ($8K) + working capital cushion ($7K). FICO 685, 2 months in business.

Recommendation: Microloan for $35K at 10.5% over 84 months. Monthly payment $589. Intermediary also provided 6 sessions of free business-planning mentorship. Bakery opened on schedule and broke even by month 5.

Second-year operating expansion

Situation: Small marketing agency with $18K/mo revenue, 580 FICO. Needed $25K to hire a second contractor and pay 3 months of upfront capacity.

Recommendation: Microloan at 11.5% APR over 60 months. Monthly $551. The expansion generated $4K/month in net new contribution by month 4. The microloan paid for itself in <8 months.

Explore SBA microloan and small-business funding options

Whether you need $10K or $5M, BizBee can match you with the right product across SBA, online, and bank-fintech partners. Soft credit pull only.

Frequently asked

Common questions

Key facts in one line

- SBA microloans offer up to $50,000 at 8–13% APR over up to 84 months.

- The average SBA microloan size is roughly $15,000.

- SBA microloans accept FICO 600+ — more flexible than standard SBA 7(a).

- Microloans CANNOT fund real estate or refinance existing debt.

- Most intermediaries provide free or low-cost business mentoring alongside the loan.

Glossary

Terms worth knowing

- Intermediary lender

- An SBA-approved nonprofit organization that originates, underwrites, and services SBA microloans using SBA-loaned capital.

- Origination fee

- Upfront fee charged by the intermediary for processing the loan, typically 1–3% of loan amount.

- Use of funds restriction

- SBA microloans cannot fund real estate purchases or repayment of existing debt — a key difference from SBA 7(a).

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.