Factor Rate vs APR

Factor rate = total cost multiplier; APR = annualized rate that accounts for time. Factor 1.30 over 12 months ≈ 55% APR. Over 18 months it's ≈ 35% APR. Convert before comparing.

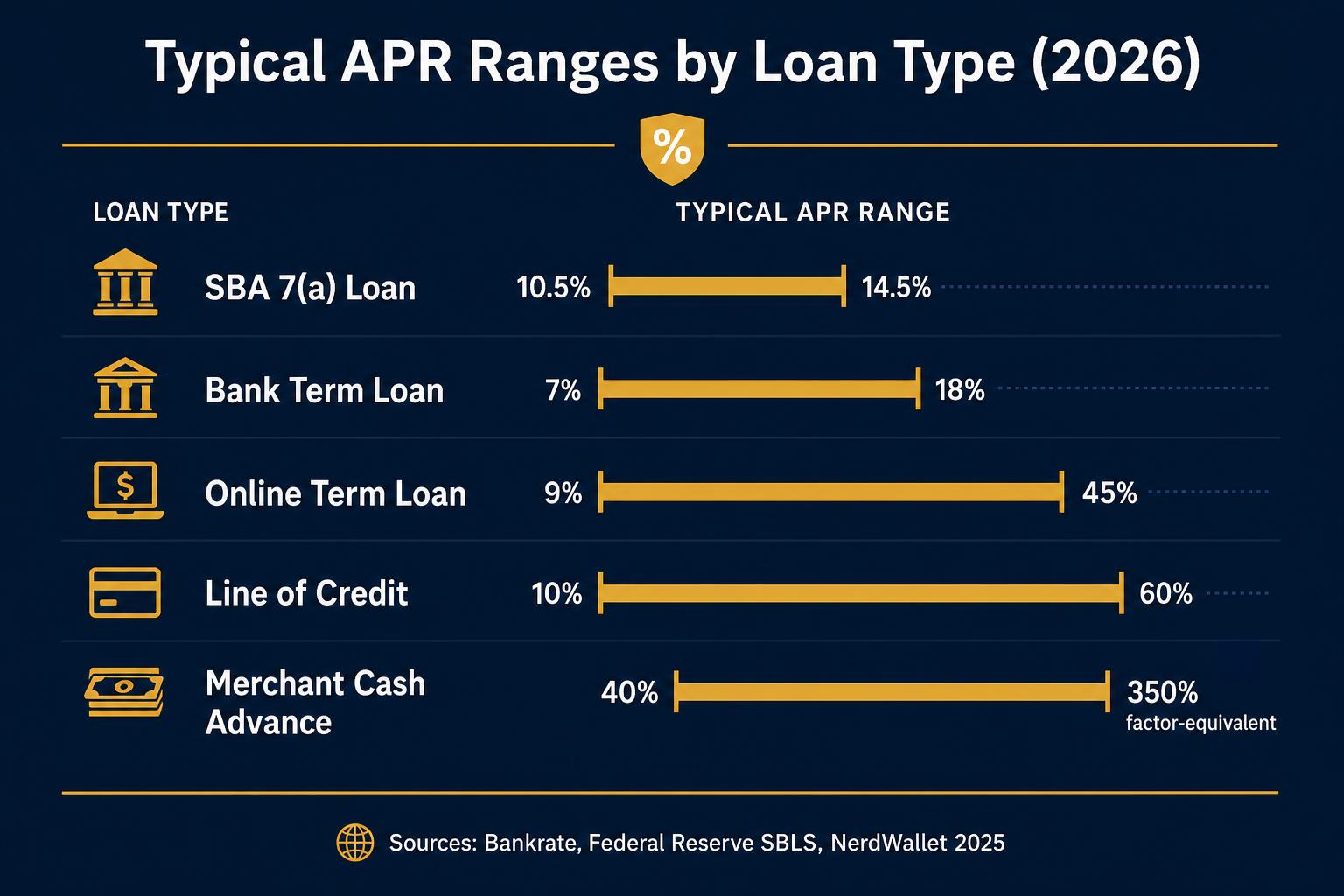

A factor rate is a flat multiplier (e.g. 1.30) applied to the funded amount, so a $50,000 advance at factor 1.30 costs $65,000 total regardless of how fast it's repaid. An APR is an annualized percentage rate that accounts for time, so a factor 1.30 paid back in 6 months has a much higher APR (~110%) than the same factor paid back over 18 months (~35%). Always convert factor rates to APR equivalent before comparing offers.

Key takeaways

- Factor rate is flat; APR is time-weighted.

- Faster repayment = higher effective APR for the same factor.

- MCAs and short-term advances quote factor; banks and SBA quote APR.

- Always convert to APR equivalent before choosing.

- Rough formula: APR ≈ (Factor − 1) × (365 / days to repay) × 100.

Who this is for

Owners weighing an MCA, short-term loan, or revenue-based offer against a bank or SBA quote.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Quoted as factor | MCAs, short-term advances, revenue-based |

| Quoted as APR | Term loans, LOCs, SBA, bank loans |

Worked example: $50K at factor 1.30

Total repaid: $65,000. Cost of capital: $15,000.

Repaid in 6 months (≈180 days): APR ≈ (0.30) × (365/180) × 100 ≈ 60.8%, but because payments amortize daily, the effective APR is closer to 110%.

Repaid in 18 months (≈540 days): APR ≈ (0.30) × (365/540) × 100 ≈ 20.3%, effective APR around 35%.

Why factor and APR are not interchangeable

A factor rate measures total dollar cost: factor 1.30 = repay 130% of advance, period. An APR measures the annualized cost of money over time. The same total dollar cost is a vastly different APR depending on whether you repay in 4 months or 18 months, faster repayment means higher APR for the same factor.

This is why MCA salespeople who say 'factor 1.30 is only 30% interest' are wrong. 30% is the total cost, not the annualized rate. A 4-month payback at factor 1.30 is roughly 90%+ APR. An 18-month payback at the same factor is roughly 35% APR. The number doesn't lie; the framing does.

When factor pricing can actually beat APR pricing

Factor-priced products (MCAs, short-term advances) can win on speed and credit flexibility, funding in 24–72 hours at 500+ FICO when APR products would reject the deal. The trade is total cost.

Factor pricing also wins on certainty: the total dollar payback is locked at funding, regardless of how slow business gets. APR products can balloon with late fees, default rates, or unexpected adjustments. For an owner who needs known dollars and known days, factor pricing has a real (if expensive) appeal.

How daily and weekly amortization distort the APR comparison

The simple conversion formula — APR ≈ (Factor − 1) × (365 / days to repay) × 100, treats the entire balance as outstanding for the full term. In reality, daily-debit MCAs collect a fixed amount every business day, so the average outstanding balance is closer to half the original advance by the midpoint of the term. This is why a factor 1.30 with a 9-month payback that 'should' equal 49% by the simple formula actually carries an effective APR of 85%–110% once amortization is modeled correctly.

Weekly-debit products behave similarly but slightly less aggressively, effective APR usually runs 20%–40% above the simple-formula number rather than 60%–80% above. Monthly-payment short-term loans are the closest to a true APR product because the outstanding balance reduces only 12 times a year instead of 250+.

The practical rule: when an MCA quote and a term-loan quote look similar by the simple formula, the MCA is almost always 40%–80% more expensive in true APR. Confirm before assuming parity. BizBee advisors run the full amortization model on every factor offer before presenting it alongside an APR offer so the comparison is honest, not just mathematically convenient.

How state disclosure laws are starting to standardize factor-to-APR comparisons

Four states, California, New York, Virginia, and Utah, now require commercial financing providers to translate factor rates into APR (or APR-equivalent) on a standardized disclosure form before a borrower signs. California's regulation (DFPI commercial financing disclosure rules, in force since December 2022) is the most prescriptive: the funder must show APR calculated under a uniform method that accounts for daily or weekly amortization, gross vs. net advance, and total fees. New York's Commercial Finance Disclosure Law (effective August 2023) is structurally similar; Virginia and Utah follow the same template.

The practical effect for borrowers is that a factor 1.30 quote in California must come with a stated APR — typically in the 60%–110% range depending on payback timing, printed on the standardized form. A funder that can't or won't produce the form for a California-based borrower is operating in violation of state law, which is itself a disqualifying signal. Borrowers in non-disclosure states should ask for the same form anyway; legitimate national funders maintain a standardized template across all states and produce it on request.

Illinois, Georgia, Connecticut, and Florida have similar legislation pending or in early enforcement as of 2026. The national trajectory is clearly toward mandatory APR disclosure on every factor-rate product, which should make honest comparison materially easier within 2–3 years.

How to decide if this is right for you

Five steps to compare any factor-rate offer against any APR offer honestly.

-

1

Get the exact total payback dollars

Advance × factor = total payback. This is the number you'll repay, period.

-

2

Get the exact payback period in days

Daily debit × business days = total days. Don't accept 'about 9 months', get the math.

-

3

Convert factor to APR equivalent

APR ≈ (Factor − 1) × (365 / days to repay) × 100. Adjust upward 30%–80% for amortization.

-

4

Compare the APR-equivalent to the APR offer

Now you have two numbers that mean the same thing.

-

5

Layer in fees and prepayment terms

Origination, draw fees, and prepayment penalties all change the real cost. Add them in before deciding.

When this makes sense

- You have at least one factor-rate offer and at least one APR offer side by side.

When to be careful

- Salespeople who say 'factor 1.30 is only 30% interest' — that's almost always wrong.

- Daily-debit MCAs with very short payback windows can hide triple-digit APRs.

How this plays out in practice

Owner comparing $75K MCA vs $75K online term loan

Situation: MCA: factor 1.30, $97.5K total, 10-month payback. Term loan: 28% APR, 24 months, $98K total payback.

Recommendation: Same total dollars, very different cash-flow profile. The MCA hits cash flow 2x as hard per month. Take the term loan unless speed is the deciding factor.

Short-term advance with implied triple-digit APR

Situation: $25K advance at factor 1.22, 90-day payback. Total payback $30.5K. APR-equivalent ≈ (0.22 × 365/90) ≈ 89%.

Recommendation: Only viable if the funded use returns more than 89% annualized, which is rare. Look for a longer-payback alternative first.

Bank LOC at 11% APR vs MCA at factor 1.25

Situation: Bank takes 4 weeks to close. MCA funds tomorrow. Need is a $40K piece of equipment that earns $1,000/day starting next week.

Recommendation: MCA. The 4-week delay costs $20K+ in foregone earnings, far more than the APR spread.

Owner reading two MCA offers with the same factor

Situation: Both offers are factor 1.28 on $80K. Offer A: 9-month payback. Offer B: 14-month payback. Same total dollars repaid ($102.4K) on both.

Recommendation: Offer B. Same total cost, but the longer payback drops effective APR from ~95% to ~50% and frees ~$2,500/mo of cash flow during repayment. Always take the longer term when total dollars are equal.

Two MCA offers with identical factor but different fee structures

Situation: Offer A: factor 1.28 on $100K with $0 origination. Offer B: factor 1.26 on $100K with a $4,000 origination fee deducted at funding (net advance $96K).

Recommendation: Offer A. Once the $4,000 fee is netted out of Offer B, the effective factor is 1.3125 on a $96K net advance — worse than Offer A's 1.28 on a $100K net advance. Always run the conversion on net advance, not gross.

Get an apples-to-apples comparison

BizBee shows every offer in APR-equivalent so you can compare honestly.

Frequently asked

Common questions

Key facts in one line

- Factor 1.30 repaid in 12 months equals roughly 55% APR equivalent.

- Factor rates do not amortize, early payoff usually does not reduce total cost.

Glossary

Terms worth knowing

- Factor rate

- A flat multiplier (e.g., 1.30) applied to a funded amount. Total cost = advance × factor.

- APR equivalent

- The annualized interest rate that produces the same total dollar cost as a given factor rate over a specific payback period.

- Effective APR

- The true annualized rate when daily/weekly amortization is accounted for. Usually 30%–80% higher than the simple APR formula suggests.

- Disclosure laws

- California, New York, Virginia, and Utah currently require commercial financing providers to disclose APR. More states are following.

- Holdback / debit percentage

- The fixed percent of daily revenue (typically 8%–20%) or the flat daily ACH amount the MCA funder collects until the factor is paid in full.

- Net advance

- The actual dollars deposited into the borrower's bank account after origination, wire, and processing fees are deducted from the gross advance. The number that should be used in the APR conversion, not the headline advance amount.

- Reconciliation right

- A contractual provision in most MCA agreements allowing the borrower to request a debit reduction when revenue materially drops. Distinct from APR but materially changes the realized cost of capital when invoked.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.