How Are Business Loan Rates Determined?

Six factors: credit, revenue, time in business, industry, product type, and the lender's own cost of funds (Prime rate). The first four are the levers you control.

Business loan rates are determined by six factors: the borrower's personal and business credit, monthly revenue and bank-deposit consistency, time in business, industry risk, the loan product itself (LOC vs term vs MCA), and the lender's cost of capital, which moves with the Fed Funds and Prime rates. Stronger inputs on the first four shift you into lower-priced product tiers.

Key takeaways

- Personal FICO is the single biggest borrower-side lever.

- Average daily bank balance often matters more than total deposits.

- Industry risk ratings can shift your rate ±5%–10% APR.

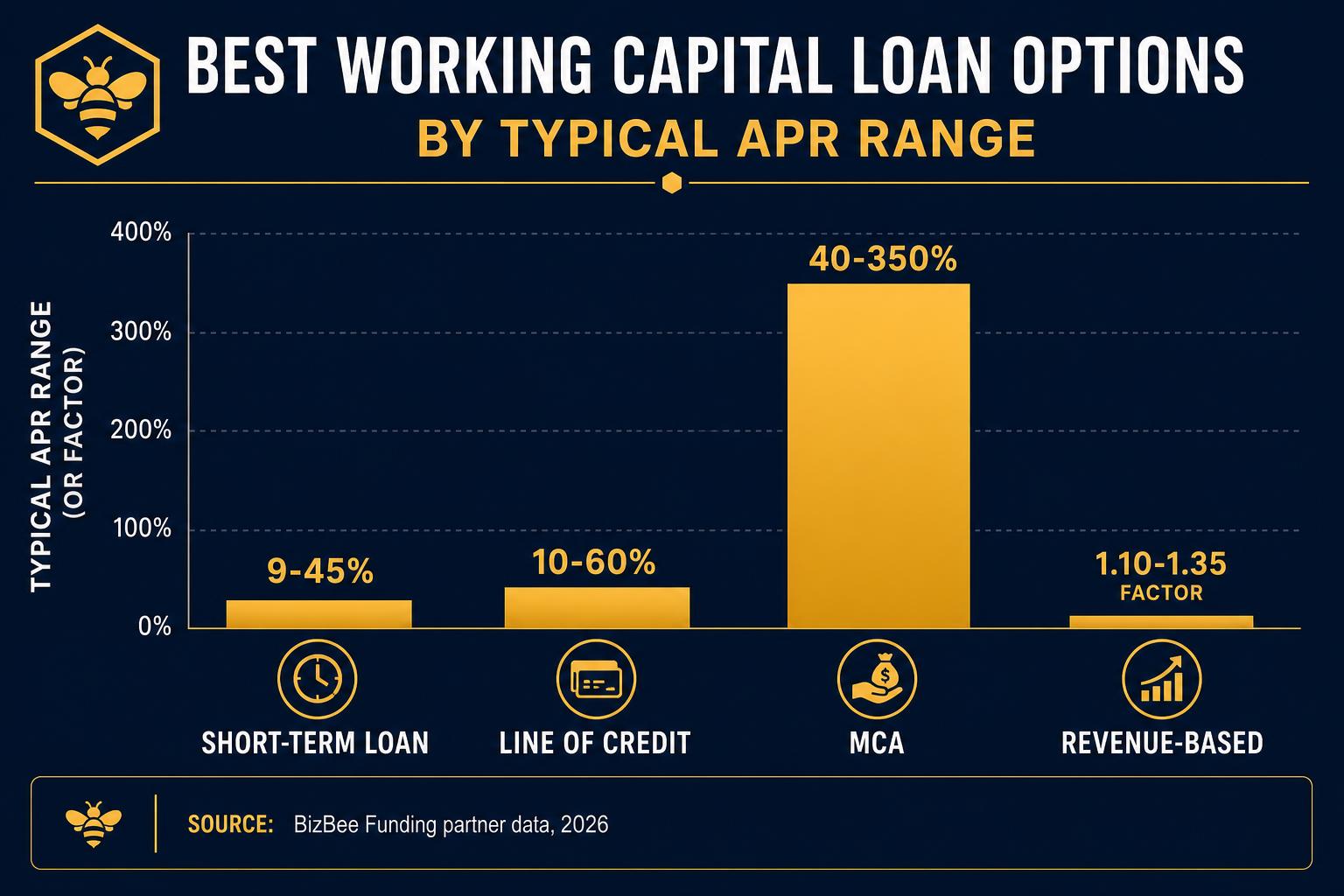

- Product type sets the price floor: LOC < term < MCA.

- Prime rate moves the entire market in 30–90 days.

Who this is for

Owners who want to know what to improve to get a lower rate next time.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Personal credit | Top 1 factor for most lenders |

| Monthly revenue | Validates ability to repay |

| Time in business | Reduces default-risk premium |

| Industry risk | Restaurants, trucking, construction priced higher |

| Loan product | Sets the rate floor |

| Prime rate | Moves the entire market |

The six factors in order of impact

1. Personal FICO, 30–40% of pricing weight.

2. Average daily bank balance & deposit consistency, 20–30%.

3. Time in business, 10–20%.

4. Industry risk rating, 5–15%.

5. Loan product chosen — sets the floor.

6. Prime rate / lender cost of funds, moves everyone.

How underwriters actually weigh your file

Online lenders run automated underwriting models that score your bank statements (deposit count, average daily balance, negative-day count, NSF count, MCA debits already present), credit (FICO, recent inquiries, revolving utilization, derogatories), and entity data (time in business, industry NAICS, state). The model spits out a tier; the tier drives pricing.

Bank and SBA underwriting layers in manual review of financial statements, tax returns, and a debt-service coverage ratio (DSCR) calculation. DSCR above 1.25 unlocks the best bank pricing; below 1.10 typically triggers decline. Improving cash flow visibility is often more valuable than improving FICO at the bank level.

The levers you can move in 30, 60, and 90 days

30 days: pay down revolving credit card balances to under 30% utilization, typically worth 10–30 FICO points and 2%–5% APR. 60 days: increase average daily bank balance by holding deposits longer before sweeps, directly affects deposit-based underwriting. 90 days: build 90 days of clean payment history on any existing debt and remove derogatory marks where possible.

These three levers consistently move a borrower from one pricing tier to the next within a quarter, often saving 5%–10% APR on the next loan.

Industry risk: why your NAICS code matters

Lenders maintain internal industry default-rate tables. Restaurants, trucking, construction, and gas stations consistently price 5%–10% APR higher than B2B services, healthcare, and e-commerce because historical default rates run 2–3x higher. Some lenders won't fund certain NAICS codes at all.

If your business straddles two industries (e.g., a contractor with a retail showroom), filing under the lower-risk NAICS code at the secretary of state level can directly improve your rate. Check with your CPA before re-filing.

How Prime, SOFR, and the lender's cost of funds set the floor

Every business loan rate is built on top of a base rate that reflects what it costs the lender to source the money. Banks and SBA loans price off Prime (currently roughly 7.00%–7.25% in early 2026 after the Fed's 2024–2025 cut cycle, per Federal Reserve H.15 data). Online term lenders typically benchmark to SOFR or to a fund-specific cost-of-capital that runs 200–400 basis points above SOFR. MCAs price off a risk-adjusted hurdle rate, not a benchmark — which is why MCA pricing barely moves when Prime moves.

Practical effect: when Prime drops 100 basis points, bank and SBA rates drop nearly 1-for-1 within 30–90 days, online term loans drop 25–60 basis points (the rest of the gap absorbs lender margin compression), and MCAs barely move. When Prime rises, the opposite plays out, bank and SBA rates climb fastest. This is why borrowers shopping in a falling-rate environment often benefit from waiting 60 days for SBA or bank quotes, while borrowers in a rising-rate environment should lock fixed-rate term loans as quickly as possible.

The Fed Small Business Credit Survey (2025) shows median bank term-loan APRs near 9.5% in early 2026 versus roughly 11% in mid-2024, confirming the Prime drop reached small-business pricing. Online term-loan medians dropped from approximately 28% to 24% over the same window, a smaller but still meaningful move.

The risk premium: how lenders quantify the cost of saying yes to you

The all-in rate equals the lender's cost of funds plus a risk premium. The risk premium is the lender's calculated probability of default times their expected loss given default, plus a profit margin. Credit, revenue, time in business, industry, and product type each get a quantified risk premium that gets added or subtracted from the base offer. Improving each input shrinks the premium.

Approximate 2026 risk-premium ranges by factor: FICO under 600 adds 8–15 APR points vs FICO 720+; under 12 months in business adds 5–12 points vs 5+ years; restaurant or trucking NAICS adds 5–10 points vs B2B services; under $20K/mo deposits adds 3–8 points vs $100K+/mo; MCA product structure adds 25–50 APR-equivalent points vs a term loan at the same credit. The premiums stack, a 580 FICO, 8-month-old restaurant with $15K/mo on an MCA can be 50–70 APR points above a 720 FICO, 5-year B2B service business on a bank term loan, even though both are 'business loans.'

The owner-side takeaway: you can't change Prime, but you can change credit, deposits, time in business, and the product you apply for. A 90-day push on credit (revolving paydown, dispute resolution) and bank-balance discipline can move you a full pricing tier and save 5%–15% APR on the next loan.

How to decide if this is right for you

Five-step playbook to move your rate down before you apply.

-

1

Pull your personal credit and dispute errors

Free at annualcreditreport.com. Disputes resolve in 30 days. Removing one derogatory can be worth 20–40 FICO points.

-

2

Pay revolving balances under 30% utilization

The single fastest credit-score move. Time it to report before applying.

-

3

Increase average daily bank balance

Hold deposits longer, delay outflows when possible. Most online lenders weight ADB heavily in underwriting.

-

4

Confirm your NAICS code is the best fit

A small classification change can unlock better pricing. Verify with your accountant first.

-

5

Apply only when your file is ready

Don't shotgun applications. Each hard pull dents your score. Pre-qualify soft-pull first.

When this makes sense

- You're planning to apply in the next 60–90 days and want to maximize your rate.

When to be careful

- Don't try to game one factor at the expense of another — paying down credit by overdrawing the bank account makes things worse.

How this plays out in practice

Borrower 30 days from applying

Situation: 640 FICO, 60% credit card utilization, $25K/mo deposits, 18 months in business.

Recommendation: Pay revolving down to 25% utilization → expect 25–40 FICO point lift → moves from 25%–35% APR tier to 18%–25% APR tier. Wait 30 days for scores to update before applying.

Bank applicant rejected on DSCR

Situation: Borrower at 720 FICO, $1.2M revenue, $80K net profit. Bank declined the $250K request citing DSCR below 1.10.

Recommendation: Either reduce the ask to a level where DSCR clears 1.25, or restructure financials with the CPA to surface owner add-backs that improve calculated cash flow.

Industry rate premium

Situation: Restaurant owner quoted 30% APR; same revenue/credit profile gets 18% APR in a B2B service business.

Recommendation: Industry premium is real and won't go away. Look for restaurant-specialist lenders (Credibility Capital, Funding Circle, etc.) who price the sector more accurately.

Borrower in a falling-rate environment timing the application

Situation: Owner with 700 FICO, $80K/mo revenue, 3 years in business, needs $200K. Fed has cut rates 75 bps in the last 6 months with another 50 bps expected in 90 days.

Recommendation: If the use of funds can wait 60–90 days, time the bank/SBA application to the post-cut window. Bank pricing follows Prime nearly 1-for-1 within 30–90 days of a Fed cut, so a 75-bp delay can save 75 bps on a $200K, 36-month loan, roughly $2,200 in interest. Online term loans move more slowly (25–60 bps per 100 bp Fed cut), so the timing benefit is smaller there. MCAs essentially don't move with the Fed, so don't wait if MCA is the only product on the table.

See your real rate, not a guess

Soft pull. 75+ lenders. No credit impact.

Frequently asked

Common questions

Glossary

Terms worth knowing

- DSCR (Debt-Service Coverage Ratio)

- Annual net operating income divided by annual debt service. Banks typically require 1.25+. Below 1.10 usually triggers decline.

- Average daily balance (ADB)

- The mean balance in the business bank account across a statement period. A primary input in online lender underwriting.

- NSF (Non-Sufficient Funds)

- A failed transaction due to insufficient account balance. More than 2–3 NSFs in a 90-day window typically triggers decline.

- NAICS code

- The North American Industry Classification System code. Lenders use it to assign industry risk premiums.

- Risk premium

- The portion of your rate above the lender's cost of capital, reflecting credit, time-in-business, and industry risk.

- Cost of funds

- What it costs a lender to source the money they lend. Banks fund at deposit rates (Prime − ~200 bps); non-bank lenders fund at SOFR + 200–400 bps from debt facilities. The floor under every loan rate.

- Pricing tier

- A bucket inside a lender's underwriting model where similar-profile borrowers receive the same rate band. Moving up one tier typically saves 3%–8% APR — and is the lever borrowers can actually move via credit and deposit improvements.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.