What Is a Good Business Loan Interest Rate?

Excellent: under 12% APR. Good online: 12%–22%. Normal short-term: 22%–35%. Above 45% only when speed matters more than cost.

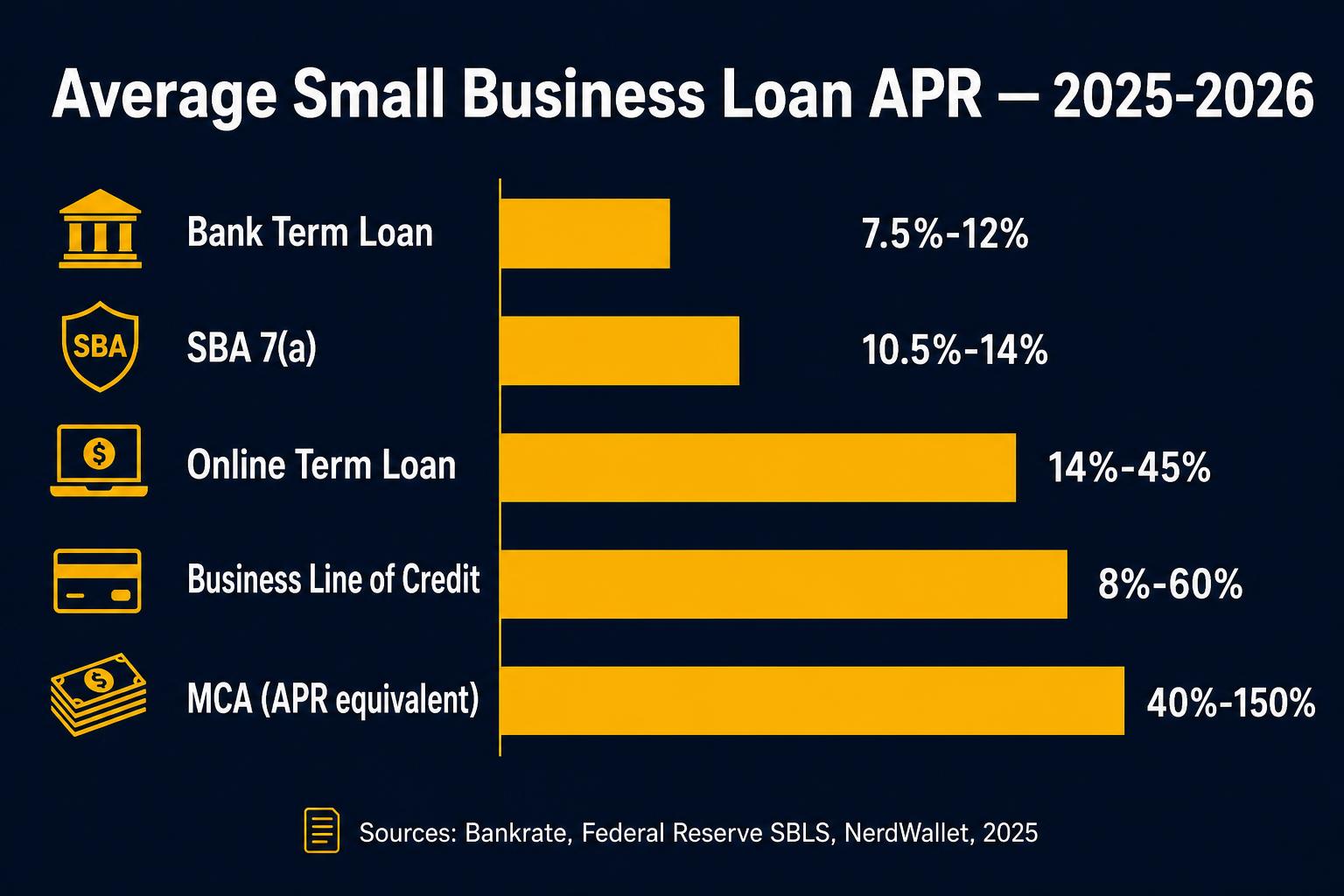

In 2026, a good business loan interest rate depends on the product: under 12% APR is excellent for any product, 12%–22% is a strong online rate, 22%–35% is typical for short-term online funding, and above 45% APR equivalent is only worth it when speed is critical. For SBA and bank loans, anything under 14% APR is considered good.

Key takeaways

- Under 12% APR = excellent for any product in 2026.

- 12%–25% APR = strong online term loan or LOC.

- 22%–35% APR = normal for short-term, fast-funding products.

- 35%–60% APR equivalent = MCA pricing — only worth it for speed.

- Compare against your business ROI, not just other offers.

Who this is for

Owners trying to decide whether the offer in front of them is fair.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Excellent | <12% APR, bank/SBA/prime online |

| Good | 12%–22% APR, established online |

| Normal short-term | 22%–35% APR |

| High but acceptable for speed | 35%–55% APR |

| Last resort | 55%+ APR equivalent |

What 'good' really means in business lending

A 'good' business loan rate in 2026 is the lowest rate available to your specific credit, revenue, and time-in-business profile, not the lowest rate in the market. A 700 FICO, $1M revenue, 5-year business should benchmark against bank/SBA rates (7.5%–13.5% APR). A 620 FICO, $20K/mo, 14-month business should benchmark against online tier (18%–28% APR). Comparing the second profile to the first is how owners get talked out of perfectly good offers.

The honest framework: under 12% APR is excellent for any borrower, 12%–22% is strong for established online borrowers, 22%–35% is normal for short-term and fast-fund products, 35%–60% APR equivalent is MCA territory (speed-priced), and anything above 60% should be a last resort with a clear ROI.

ROI math: when a 'high' rate is still a good deal

Rate alone isn't a deal-killer. A 30% APR loan funding a use that returns 70% is a great deal. A 9% APR loan funding a use that returns 5% destroys value. The right comparison is rate vs ROI on the funded use, not rate vs other rates.

Quick ROI test: (Net dollars added by funded use over loan term) ÷ (Loan principal + total interest + fees). If that ratio is greater than 1.5x, the rate is good for that specific use. If it's under 1.1x, rethink the loan even at low APR.

Where lenders quietly raise rates without telling you

Quoted 'rate' often excludes origination, draw fees, wire fees, and prepayment penalties. A 14% APR with 5% origination on a 12-month loan is closer to 19%–20% all-in. Daily-debit products often quote an APR that doesn't account for amortization speed — effective APR can be 30%–80% higher than quoted.

Always get all-in APR in writing, with every fee enumerated, before deciding whether a rate is good.

How the 2026 rate environment changes what 'good' means

The Federal Reserve's 2024–2025 rate-cut cycle pulled Prime from 8.50% to roughly 7.00%–7.25% by early 2026, which dropped bank and SBA pricing by about 1.5 APR points across the board. The Fed Small Business Credit Survey shows median bank term-loan APRs near 9.5% in early 2026 versus roughly 11% in mid-2024. Online lenders followed but moved less, typical online term-loan APRs dropped from 28% to about 24%, and MCA factor pricing barely moved because factor pricing is tied to risk and speed, not Prime.

Practical effect on the 'good rate' benchmark: a rate that was 'good' in 2023 (say, 16% on an online term loan for a mid-tier borrower) is now merely 'average.' Owners should renegotiate or refinance any active loan that's more than 12 months old and priced above the current tier benchmark, the savings are often $3K–$15K per $100K of remaining balance over the rest of the term.

Rate environment also affects whether to lock or float. Fixed-rate term loans protect against future Prime increases but lose value if Prime keeps falling. Variable-rate LOCs win in a falling-rate environment but hurt if rates reverse. The current consensus among BizBee's lending partners is that Prime is unlikely to drop materially below 6.5% in 2026, so fixed-rate term loans at sub-13% are worth locking now.

How to negotiate a quoted rate down by 2–5 APR points

Almost every online and bank lender prices new loans with built-in negotiation room. The published or initially-quoted rate is rarely the lender's actual best price. Borrowers who negotiate well typically save 2–5 APR points on the same loan, which translates to thousands of dollars on a typical $100K loan over a 36-month term. The negotiation works because lenders compete intensely on funded volume and would rather discount a deal than lose it to a competitor.

Three tactics produce most of the savings. First, get a written competing offer before negotiating, even one competing quote at a comparable structure shifts pricing power. A lender that wouldn't budge from 18% APR on the original quote will frequently drop to 15% APR when shown a competitor's 14% APR offer. Second, ask explicitly for the 'best and final' rate and confirm in writing — many lenders quote a 'good' rate first and reserve a better rate for borrowers who push back. Third, negotiate fees alongside rate, origination fees, doc fees, and prepayment penalties are all individually negotiable, and concessions on fees are often easier for the lender to grant than rate concessions.

What doesn't work: emotional appeals, threats to leave reviews, or asking for discounts without a competing offer. Lenders are running underwriting math, they respond to data (competing offers, strong credit profiles, willingness to add personal guarantee or collateral) rather than pressure. The best-prepared borrowers walk into the conversation with two or three written competing offers, current bank statements, an updated personal credit report, and a clear question: 'What is your best rate to win this deal?' That question, asked with competing data behind it, reliably saves more than any other single move a borrower can make.

How to decide if this is right for you

Five questions decide whether a quoted rate is good for your situation.

-

1

Identify your borrower tier

FICO + time in business + revenue puts you in prime, mid, or short-term. The benchmark range follows from the tier.

-

2

Get all-in APR in writing

Headline rate + fees annualized = real cost. Without this number, no rate is verifiable.

-

3

Compute ROI on the funded use

Net profit added over the loan term ÷ total cost of capital. Above 1.5x = green light.

-

4

Benchmark against your tier, not the market

A 25% APR is great for a 620-FICO 14-month business. The same rate is overpriced for a 720-FICO 5-year business.

-

5

Get a second offer before accepting

Even one competing quote typically saves 2%–5% APR via negotiation.

When this makes sense

- You have a written offer and a clear use of funds.

- Your projected ROI on the funded use beats the loan's cost.

When to be careful

- Comparing apples to oranges, always convert MCAs to APR equivalent first.

- Taking a 'good' rate on a loan you don't actually need.

How this plays out in practice

Mid-tier borrower considering 22% online term loan

Situation: 650 FICO, 24 months in business, $40K/mo revenue. Quoted 22% APR all-in for $75K, 36 months.

Recommendation: Solid offer for the tier. Negotiate to 19%–20% with a competing quote. Accept if no better arrives in 48 hours.

Prime borrower considering 16% online term loan

Situation: 720 FICO, 4 years in business, $90K/mo revenue, no prior business debt. Online lender quotes 16% APR.

Recommendation: Overpriced for the tier. This profile should qualify for 9%–12% APR at a bank or 11%–14% APR at SBA. Walk and shop the better-tier products.

Fast-need borrower considering 50% APR MCA

Situation: Owner needs $30K in 48 hours for a confirmed $90K contract netting in 60 days. Only offer is factor 1.28 (~50% APR equivalent).

Recommendation: Good deal. Contract ROI ($60K profit / $8.4K MCA spread) is 7x cost. Take the speed-priced capital.

Established borrower with old high-rate debt

Situation: 680 FICO, 5 years in business, $80K/mo revenue, currently 18 months into a 36-month online term loan at 28% APR. $65K balance remaining.

Recommendation: Refinance. Current tier qualifies for 14%–17% APR. Refinancing at 15% saves roughly $7,800 in interest over the remaining 18 months. Confirm no prepayment penalty before pulling the trigger.

Borrower comparing two offers with different origination structures

Situation: Offer A: 16% APR with 0% origination on $100K, 36 months. Offer B: 14% APR with 5% origination on $100K, 36 months.

Recommendation: Run all-in APR on both. Offer A all-in ≈ 16% (no fee to amortize). Offer B all-in ≈ 17.3% once the $5,000 origination is amortized across 36 months. Offer A wins by roughly $2,000 in total cost despite the higher headline rate. Always run all-in APR, headline rate alone is misleading.

Get benchmarked offers in minutes

BizBee shows every offer in APR-equivalent so you know if it's good.

Frequently asked

Common questions

Glossary

Terms worth knowing

- Borrower tier

- The pricing band you fit into based on FICO, time in business, revenue, and industry. Tiers are how lenders match rate to risk.

- All-in APR

- The annualized rate including origination, draw, wire, and prepayment costs. The only honest cross-lender comparison metric.

- ROI on funded use

- The net dollars the loan-funded activity produces over the loan term, divided by the total cost of capital.

- Prime rate

- The benchmark large banks charge their best customers. SBA, bank, and many online loans price off Prime + a credit spread.

- Credit spread

- The number of APR points a lender adds above Prime (or above their cost of funds) to price risk. Tier improvements typically shrink the spread by 2–5 points.

- All-in APR

- The annualized rate including origination, draw, wire, and prepayment costs amortized across the loan term. The only honest cross-lender comparison metric.

- Yield spread premium

- Additional commission paid to a broker for placing a borrower at a higher rate than they qualified for. Reputable brokers and marketplaces do not accept it.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.