Working Capital Loan vs Line of Credit

Working capital loan = one-time lump sum, fixed payback. Line of credit = revolving, pay interest only on what you draw. Lump sum for one big need, LOC for recurring gaps.

A working capital loan delivers a one-time lump sum repaid over 3–24 months on a fixed schedule, best for a specific known expense. A business line of credit gives a revolving credit limit you can draw from, repay, and re-draw as needed, best for recurring or unpredictable cash-flow gaps. Working capital loans typically fund faster and accept weaker credit; lines of credit usually cost less but require stronger qualifications.

Key takeaways

- Working capital = lump sum, fixed schedule, faster, lower bar.

- Line of credit = revolving, draw on demand, lower rate, higher bar.

- WC loans approve at 550+ FICO; LOCs usually want 650+.

- WC funds in 1–3 days; LOCs in 1–7 days once approved.

- LOCs only charge interest on drawn balance — better for irregular needs.

Who this is for

Owners with a cash-flow gap deciding which structure fits the need.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Working capital loan | 550+ FICO, 6+ months, $15K+/mo |

| Business line of credit | 650+ FICO, 12+ months, $25K+/mo |

How the two products actually behave in a real cash crunch

A working capital loan delivers a one-time lump sum and locks in a fixed daily, weekly, or monthly payment for 3–24 months. Once funded, the obligation is set, pay it down on schedule until done. A business line of credit gives an approved limit you can draw from anytime. Each draw layers a short repayment schedule, and as principal repays, available credit restores. The structural difference is one-time vs revolving, and it drives every other comparison.

Cost-wise, LOCs win for recurring or partial-draw use because interest accrues only on the drawn balance. Working capital loans win for one-time, fully-deployed use because the headline rate is often lower than a fully-drawn LOC of equivalent size at the same credit tier.

Approval differences that matter

Working capital loans typically approve at 550+ FICO, 6+ months in business, $15K+/mo revenue. LOCs typically want 650+ FICO, 12+ months, $25K+/mo. The bar is meaningfully higher for LOCs, which is why owners who 'want a LOC' often end up with a working capital loan as their first product, then graduate to a LOC after building 12+ months of payment history.

Funding speed: working capital funds in 1–3 business days. LOCs take 1–7 days for initial approval and limit assignment, but subsequent draws hit the bank same-day or next-day. For a true one-time emergency, working capital is faster. For ongoing readiness, the LOC's reusability makes it the faster long-term tool.

What the cost difference looks like in real dollars

Example: $50K need, recurring use across 12 months. Working capital loan at 25% APR, 12 months = roughly $7,000 in interest if fully drawn day one and amortized down. LOC at 20% APR, drawing the same $50K incrementally and repaying as cash flow allows = roughly $3,500–$4,500 in interest because average outstanding balance is lower.

Same need, different deployment, $2,500+ savings on the LOC. The trade is the higher qualification bar and slightly slower first approval.

Payment cadence and the cash-flow profile of each product

Working capital loans typically use daily or weekly ACH debits on the short-term end (3–12 month products) and monthly amortization on the longer end (18–24 month products). Daily-debit working capital on a $50K loan at 28% APR with a 10-month term pulls roughly $250 per business day from the operating account, a meaningfully heavier short-term cash-flow burden than the same loan's all-in cost suggests. Modeling the daily debit against your worst-week revenue is the single most important check before signing a daily-debit working capital product.

LOC payment cadence is more flexible. Bank LOCs typically bill monthly with interest-only minimum payments, leaving principal repayment on your schedule. Online LOCs more often bill weekly with fixed principal + interest amortization per draw — closer to a working capital loan in cash-flow profile, but with the revolving benefit of restored credit as principal repays. A few online LOCs use daily debit; treat those like working capital products for cash-flow modeling.

Practical implication: a borrower with smooth, predictable revenue can absorb daily-debit products easily and benefit from the slightly lower headline rates they offer. A borrower with lumpy or seasonal revenue should prioritize monthly or weekly billing, the cash-flow flexibility is often worth 2–4 APR points of additional cost.

The graduation path: how owners typically move from one to the other

Most owners enter the lending market with a working capital loan because the bar is lower and approval is faster. After 6–12 months of clean payment history, the same borrower typically qualifies for a LOC at improved pricing. The natural progression, short-term working capital → longer-term working capital → first LOC → larger LOC with limit increases, usually takes 18–36 months and ends with a borrower holding a LOC as their primary working-capital tool plus occasional term loans for specific large purchases.

Owners who skip the working capital step and apply directly for a LOC at 6–12 months in business often see declines, then have to wait 90+ days before reapplying. The faster path for most under-12-month businesses is a small working capital loan first (build payment history), then a LOC at month 14–18 after the working capital loan has 6+ on-time payments on file. Lenders weight in-place payment history heavily on LOC underwriting.

Combining both products: when it actually makes sense

Established businesses (3+ years, $50K+/mo revenue, 680+ FICO) frequently hold both a working capital loan or term loan for a discrete capital expenditure (equipment, renovation, acquisition) plus a LOC for ongoing operating flexibility. The combination works because the products serve different needs, fixed payback for the capex, revolving capacity for working capital — and lenders generally underwrite both as long as total debt service stays within DSCR limits (typically 1.25+).

Risk to manage: stacking products at lenders who don't know about each other is a contract breach in most agreements. Disclose all active business debt on every new application, and confirm with each lender that their underwriting allows the additional product before signing. BizBee advisors maintain a debt-stack view across the partner network to prevent inadvertent breaches.

What this typically costs

Typical 2026 cost ranges for each product.

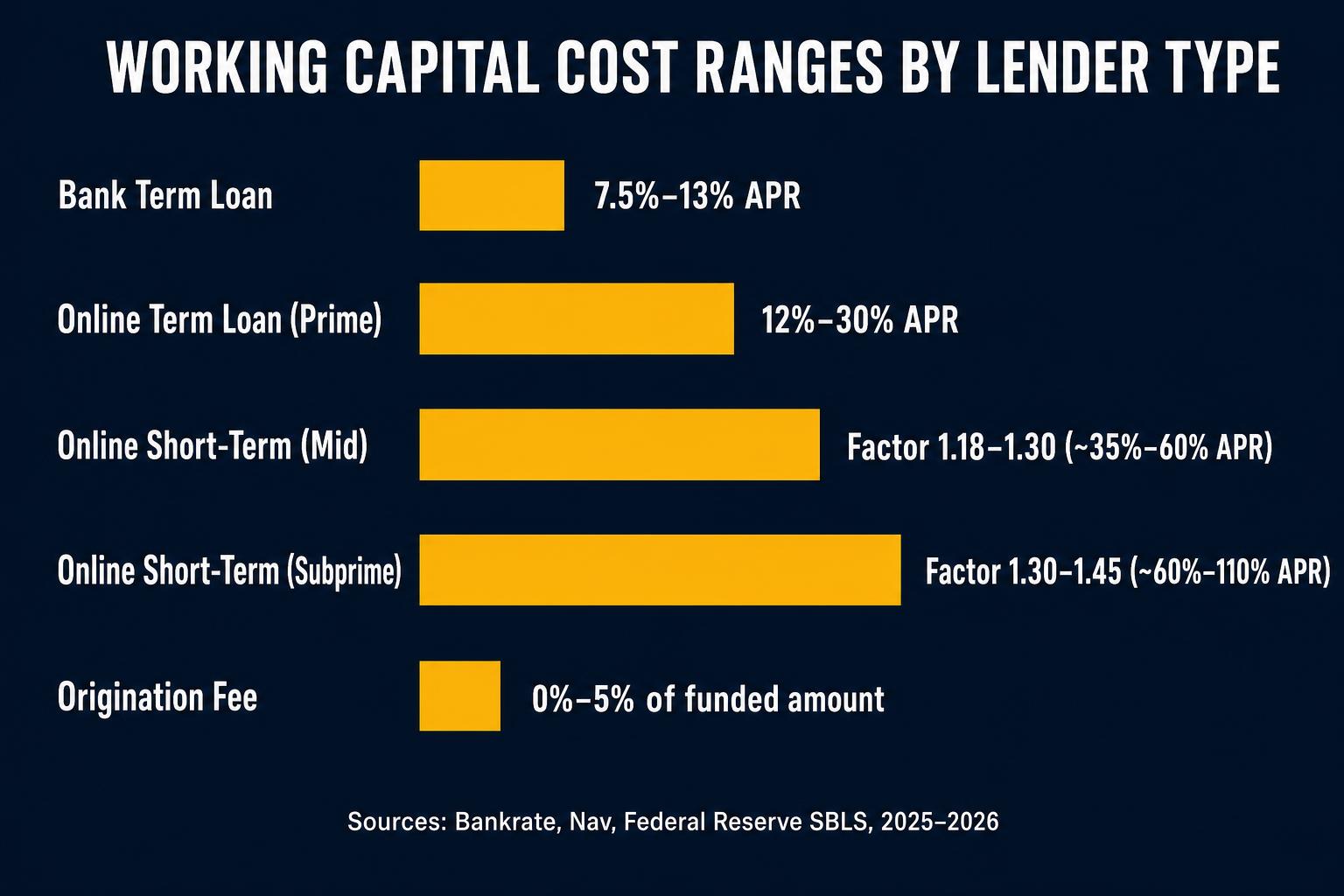

| Working capital loan | 15%–35% APR or factor 1.18–1.40 |

| Line of credit | 8%–28% APR (bank to online) |

How to decide if this is right for you

Five questions decide which product fits your specific cash-flow need.

-

1

Is the use one-time or recurring?

One-time, fully deployed = working capital loan. Recurring or unpredictable = LOC.

-

2

Do you qualify for both?

Under 650 FICO or under 12 months = working capital is your main option. Above both = LOC is on the table.

-

3

Will you deploy 100% of the funds immediately?

Yes = working capital can be cheaper. No = LOC almost always wins on interest.

-

4

How fast do you need first dollars?

Both fund in 1–7 days. For true emergencies, working capital is slightly faster on first dollar.

-

5

What's your 12-month plan?

Need future flexibility? LOC. Need a single discrete payback? Working capital.

When this makes sense

- WC loan: one specific purchase or expense you can repay on a fixed schedule.

- LOC: recurring or seasonal gaps where flexibility matters more than total amount.

When to be careful

- Don't use a WC loan as standing capital, fixed payments will eventually squeeze you.

- Don't max out a LOC and treat it like a term loan.

How this plays out in practice

One-time equipment purchase

Situation: Owner needs $40K to buy a piece of equipment with a clear 24-month payback. 660 FICO, 18 months in business, $30K/mo revenue.

Recommendation: Working capital loan. Fixed payback matches the use; lump sum simplifies the purchase; no benefit from revolving access.

Recurring seasonal inventory cycles

Situation: Retail owner buys $20K of inventory 4x per year on an irregular timeline. 680 FICO, 3 years in business, $50K/mo revenue.

Recommendation: LOC. Draw $20K each cycle, repay between cycles, only pay interest on outstanding. Saves roughly 40% on annual cost of capital vs holding a $40K WC loan year-round.

New business under tight qualification

Situation: 8-month-old business at 590 FICO, $18K/mo revenue, needs $25K to cover a payroll gap.

Recommendation: Working capital loan or short-term advance, LOC not yet available at this tier. Plan to refinance into a LOC after 12+ months of clean payment history.

Compare both side-by-side

BizBee can show you offers for both products at the same time.

Frequently asked

Common questions

Glossary

Terms worth knowing

- Lump-sum funding

- A one-time disbursement of the full loan amount at closing. Defining feature of working capital and term loans.

- Revolving credit

- A credit limit that can be drawn, repaid, and re-drawn multiple times without re-applying. Defining feature of a LOC.

- Fully drawn

- When a LOC borrower has used 100% of the approved limit. At full draw, total interest can rival or exceed a term loan of equivalent size.

- Available credit

- The portion of a LOC limit not currently drawn. Restores as you repay principal.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.